Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFTSE 100: How much can you make on each stock this year?

The FTSE 100 index has increased by nearly 14% in value since the Brexit vote on 23 June 2016 and hit a record high in early January 2017 as it broke through the 7,200 level.

Investors are understandably starting to ask if they should take profit in UK large caps. Our view is ‘no’; now is not the time to sell.

Our research shows more than a third of FTSE 100 stocks are expected to appreciate by at least 10% this year; a large handful could well rise by 20% or more.

In this article we reveal the companies whose shares prices are expected to rise the most, according to price targets calculated by analysts across a range of investment banks and stockbrokers.

We also flag the stocks with the most to lose; and we discuss where current market expectations appear out-of-kilter with underlying fundamentals, in our view.

RECORD BREAKER

It is less than a month since the FTSE 100 index broke new records, closing at 7,337.81 on 13 January following a stunning 14-day unbroken run of rises. That’s its longest winning streak in 20 years.

Having initially fallen on the EU referendum result and hitting 5,982.2 on 27 June 2016, the FTSE 100 subsequently rallied by 22.7% to its peak level on 13 January.

It is rare for the index of UK’s 100 largest firms to sprint so fast. That kind of return is more associated with small cap stocks or even the mid cap FTSE 250 index.

FUEL FOR THE FIRE

Several factors have fed this share buying frenzy. The index’s performance is heavily influenced by natural resources companies who account for some of the FTSE 100’s biggest weightings. A recovery in commodity prices last year resulted in substantial share price gains from oil, gas and mining firms.

The plunging pound since Britain decided to leave the EU also had a big impact.

Sterling has lost about 16% of its value versus the dollar since the Brexit vote, and is down against other currencies such as the euro too.

This is positive for the FTSE 100 since most of the companies within the index are very large and very global.

More than 70% of FTSE 100 companies’ earnings come from overseas, so they get a boost from translating foreign denominated earnings back into sterling or when you can consider their share prices are nearly all priced in sterling.

So has the FTSE 100 become expensive on the back of its recent rally? According to data from Morningstar, the index trades 15.6 times earnings. That is roughly in line with long-run averages and certainly not excessively inflated.

The longer term track record also implies the FTSE 100 has not raced ahead into bubble territory. The FTSE 100 has gone up by 18% since the start of 2007. Adjusting for inflation, that return becomes -9.4%. Admittedly that includes one of the worst periods for the stock market in living memory thanks to the global financial crisis in 2008.

BEST MONEY MAKING OPPORTUNITIES

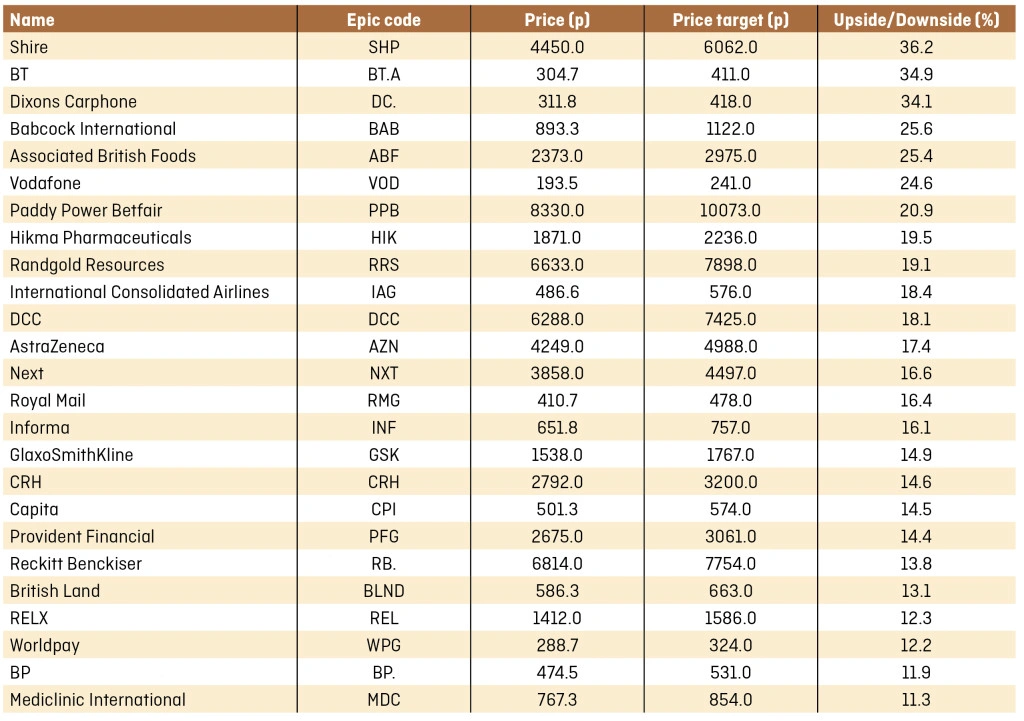

We’ve pulled together all the price targets from the analyst community to see where the best opportunities lie in the FTSE 100 for the year ahead.

Analysts produce price targets using different calculations such as equity valuations for the peer group and discounted cash flow models. They aren’t simply picking numbers out of thin air.

That said, share price targets alone are seldom accurate gauges of future performance, hence why we have undertaken extensive extra research for this article.

We now discuss the four stocks with the biggest share price upside in 2017, based on consensus price targets. We also highlight several companies where we feel there is imbalance between the market’s expectations and likely future performance, both good and bad.

Shire (SHP) £44.50

Shire has been one of the biggest success stories on the UK stock market over the past decade, thanks to its entry into the rare diseases space.

Analysts think your money could increase by more than a third this year by investing in the shares. That’s great, so why are the shares trading on such a cheap rating?

A forward price to earnings (PE) ratio of 10.8 is surprisingly low for a blue chip company that’s enjoyed rapid growth.

The rating suggests investors may have some doubts about the business or expect slower earnings growth in the future. Its dividend yield is not ideal for income hunters at a mere 0.5%.

There are several reasons why it trades on a fairly low rating. Firstly, Roche’s (ROG: VTX) haemophilia A drug ACE190 is a looming competitive threat. Shore Capital analyst Dr Tara Raveendran expects a ‘rapid erosion in Shire’s haemophilia division over the next few years’.

Secondly, investors have a mixed view towards Shire’s $32bn acquisition of Baxalta in 2016 due to sustainability concerns over its haematology division.

Baxalta could actually be Shire’s saviour as it is one of the leading companies in the $14bn plasma products markets. Raveendran says there is increasing demand for plasma-derived primary therapies and believes Shire can take advantage of new trends by delivering drugs less invasively. (LMJ)

BT (BT.A) 304.7p

The key question for BT investors is whether the company can afford its hefty dividend payments in the face of several challenges and drains on its cash flow.

Recent news regarding the £530m black hole within the books of its Italian business is uncomfortable but may not prove disastrous to the overall investment case.

Importantly, investors will want to feel that no other hidden nasties will emerge in the future.

Some analysts have speculated that the group’s bleakly-worded warning on 26 January had an ulterior motive, namely to show BT’s weakest possible hand as it continues negotiations with watchdog Ofcom over the future of its Openreach infrastructure network.

That may imply that BT has done a ‘kitchen sink’ job, throwing in all the bad news it could find to bolster its negotiating position.

The group’s considerable pension deficit remains an ongoing drain on cash resources. Top-up payments agreed with the scheme’s trustees of around £600m a year look comfortable versus the £3.1bn of free cash flow anticipated by analysts in the financial year to 31 March 2017. That free cash flow figure should nearly hit £4.2bn by 2019.

The £1.6bn-odd cash needed to pay next year’s (to March 2018) dividend looks well underpinned, in our view. (SF)

Dixons Carphone (DC.) 311.75p

We have a positive stance of Dixons Carphone as an investment, albeit we are also mindful of some swirling headwinds.

The company owns a variety of brands including Carphone Warehouse, CurrysPCWorld and a few overseas names that may not be familiar to UK households.

Shares in the group were hard hit by the Brexit vote and have struggled ever since amid concerns surrounding consumer demand and worries that weak sterling will necessitate price hikes.

The good news is chief executive Seb James recently reported (24 Jan) a fifth consecutive year of Christmas growth. That’s positive given the second half of its financial year (November to April) typically accounts for two thirds of group profit.

Dixons needs to sustain positive sales momentum if it stands any chance of pushing the share price back upwards.

Strong European market share, a compelling multi-channel proposition, overlooked potential in the business-to-business Connected World Services (CWS) division and rolling out US stores with mobile network operator Sprint (S:NYSE) are tenets of our ‘buy’ thesis. The shares also trade on a low rating.

For the year to April 2017, Numis Securities forecasts £482.5m (2016: £447m) pre-tax profit and a 10.8p dividend, rising to £500m 11.5p respectively next year. (JC)

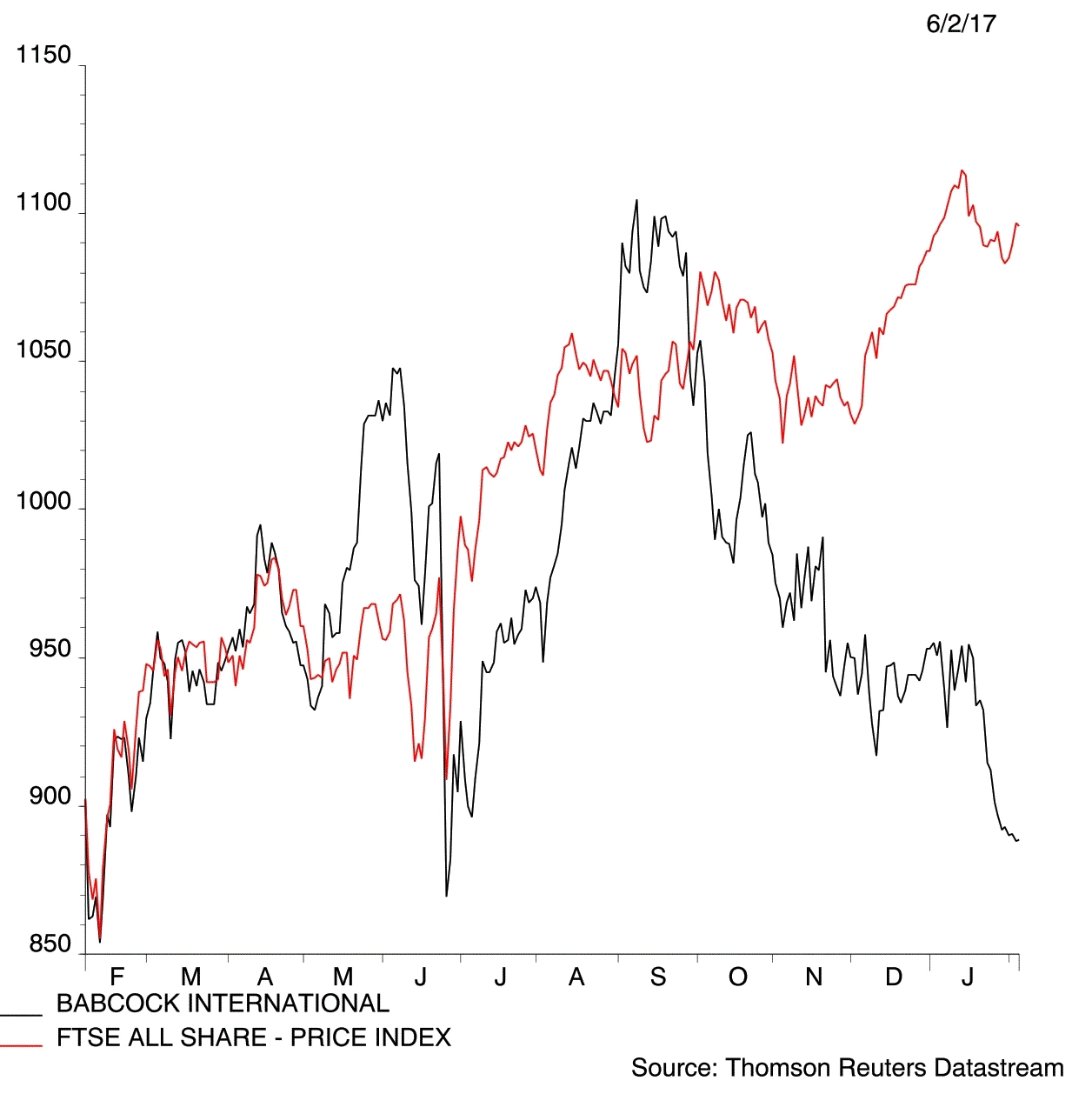

Babcock (BAB) 893.25p

Pressure on UK defence spend, a key area for Babcock, plus an ill-timed foray into the oil and gas market through its £1.6bn (over-priced) acquisition of helicopter firm Avincis have contributed to the share price weakness.

The support services group now trades on a March 2018 earnings multiple of just 10.4 times.

The valuation looks too low given the level of visibility on future revenue. An order book of £20bn underpins 93% of budgeted revenue in the current financial year and 63% in the year after.

Opportunities include the decommissioning of nuclear sites in the UK and the construction of a new plant at Hinkley Point. There is scope to expand its overseas operations and exposure to a recovering defence market.

On the downside we note poor cash conversion and substantial pension liabilities.

‘Babcock is a diverse business with a firm contractual base, supporting essential infrastructure,’ says Shore Capital. ‘The outlook for news flow looks positive.

‘Both nuclear new build and decommissioning contracts are in flow this year,’ it adds. ‘We are about to embark on a major rail upgrade and construction programme. The contracts for the new aircraft carriers are moving into the support phase and the build work is being replaced. The deployment of the UK’s armed forces does not appear to be going into a quiet period anytime soon.’ (TS)

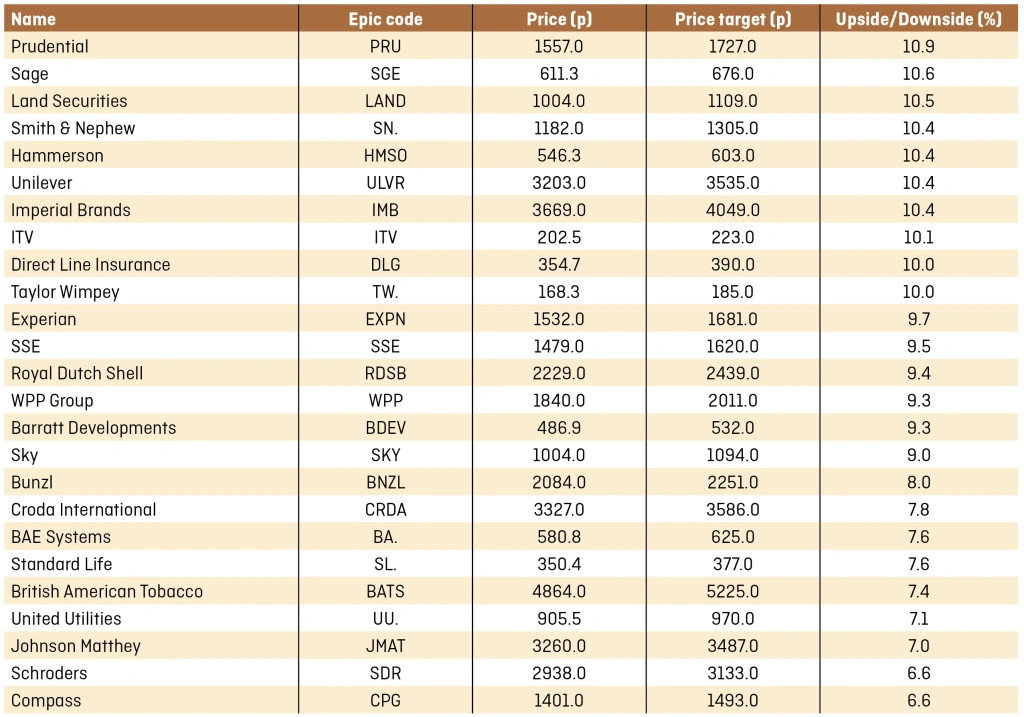

WHAT ABOUT THE REST OF THE FTSE 100?

We don’t think the share price decline has fully played out at academic publisher Pearson (PSON) and think the consensus view among analysts is too generous by saying the shares are now fairly valued at 636.3p.

Diminishing demand for hardback academic titles has led to a series of profit warnings. Investment bank Liberum, whose consistently bearish stance on the stock has proved correct, recently reiterated its ‘sell’ recommendation with a 360p price target and says it expects full year results on 24 February to reveal further issues around cash flow and write downs.

Taking profit on CRH

Construction group CRH (CRH) has enjoyed a significant share price rally since the Brexit vote as it is a clear beneficiary of a weaker pound, thanks to deriving a good chunk of its earnings from abroad. The shares got another leg up in late 2016 when Trump was elected. The US president’s plans to boost domestic infrastructure spend clearly plays to CRH’s strengths.

Investors now need to decide whether all this good news is priced in, particularly as the shares have now risen by more than 35% since the Brexit vote in June 2016.

We think the shares could pause for a while and would suggest you take some profit in the stock at £27.92. So many people are talking about CRH being a beneficiary of Trump’s plan – if everyone is talking about it, the easy money must surely have already been made on the stock.

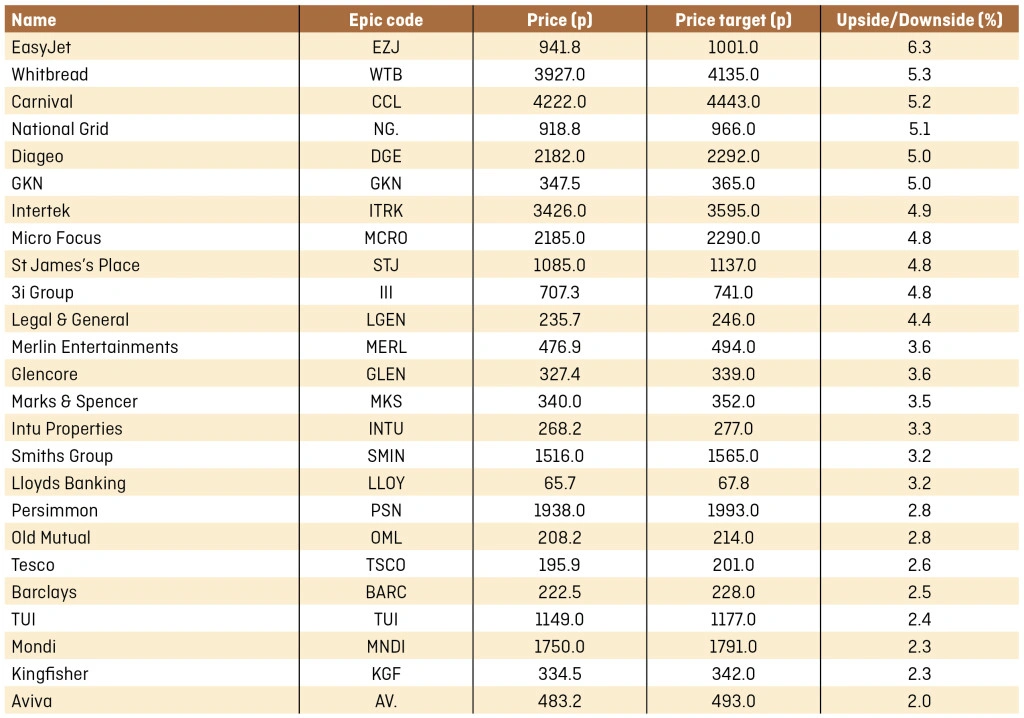

Why analysts are bearish on Antofagasta

It is hard to get excited about miner Antofagasta (ANTO), so we aren’t surprised it is at the bottom of the pile in terms of anticipated share price returns for 2017.

The company’s guidance for the year ahead implies limited or no growth in copper production and rising costs. It has disappointed on the operations front and analysts say it is going to cost a lot of money to develop Antofagasta’s future pipeline to replace old projects.

We see much greater share price upside in fellow copper miner KAZ Minerals (KAZ).

Red flags at Vodafone?

Mobile network giant Vodafone (VOD) is one stock that splits opinion and that’s largely because the strain on its cash flow. Is the dividend at risk of being cut?

The market is clearly nervousness given the stock has a 6.6% prospective yield. Seldom do FTSE 100 companies trade on such generous income ratios. Vodafone has historically had a prospective dividend yield more in the 5% range.

We continue to side with Vodafone optimists, believing that earnings recovery across Europe is being underestimated, as is the scope for M&A to add value down the line.

Kingfisher concerns

Analysts are too optimistic over B&Q-owner Kingfisher (KGF), in our view. Rival Homebase’s new owner is the deep-pocketed Wesfarmers (WES:ASX), the brains behind admired Australian hardware retailer Bunnings. Wesfarmer’s plan to spruce up Homebase stores will increase competition for B&Q in DIY hardwear, garden and seasonal ranges.

Investment bank Haitong is also not a fan of Kingfisher. It believes Kingfisher’s shares are only worth 270p versus 334.45p trading price at the time of writing. (TS/DC/JC/SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.