Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCello has US biotech opportunity in its sights

An oversubscribed fundraising (1 Feb) reflects healthcare marketing play Cello’s (CLL) scarcity value as means of gaining exposure to an attractive US pharmaceutical and biotechnology industry.

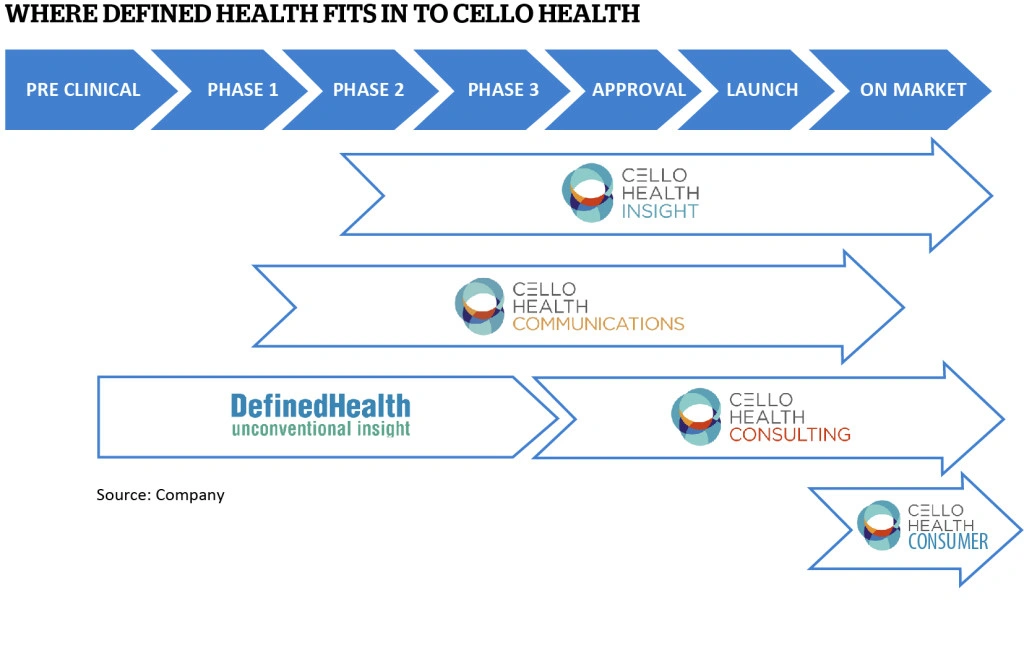

The company raised £15m at 97p (a modest discount to the prevailing share price) alongside the $5.75m (£4.6m) acquisition of US biotech consultancy Defined Health.

SHARES IN DEMAND

The company did not need to raise funds for the deal as it has limited debt on its balance sheet. However, it did so as a way of broadening its investor base and raising funds for further acquisitions which can accelerate growth ambitions across the Atlantic.

Cello has two divisions: Cello Health and Cello Signal. Revenue-wise the split is roughly 50:50 but the Health arm delivers significantly better margins and therefore accounted for around 70% of first half operating profit.

The marketing group trades on 12.5 times forecast earnings for the current financial year. That’s based on broker Cenkos’ estimates which factor in the impact of the acquisition and the placing of new shares.

Cenkos analyst James Fletcher comments: ‘It is expected that revenue synergies will be extracted from the acquisition, as Cello cross-sells Cello Health Consulting services to Defined Health’s customer base and vice versa, as well as the other disciplines of Insight, Communications and Consumer services.’

Cello chief executive Mark Scott says future acquisitions, like Defined Healthcare, will be focused on building exposure to US biotech in a market he says remains highly fragmented. By building scale Scott reckons the business can win more work from US healthcare businesses in the domestic market where the contracts are typically larger.

ACQUISITIONS PLAN

Scott is mindful that acquisitions are capable of destroying value as well as creating value. He says: ‘We’re very cautious. Unless we know the company and people in question quite well we would be reticent (to acquire a business) and we’re not prepared to participate in an auction. We also need to ensure there’s a managerial fit and no client conflict.’

The company’s increasing exposure to the US could be translate into a currency boost when it reports full year results on 22 March. There may also be an update on M&A plans alongside these numbers.

FinnCap has a price target of 132p implying upside of just over 30% at the current 101p. Progress in boosting its US presence should act as a catalyst for the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.