Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDial up Vodafone dividends

Stiff competition across Europe, a fierce price war in India and new spectrum investment demands on cash flow are putting Vodafone (VOD) dividends under scrutiny, one of the main reasons that thousands of investors and funds own the stock.

Yet analysts remain largely positive on the shares, arguing that the market has the balance between risk and return out of kilter.

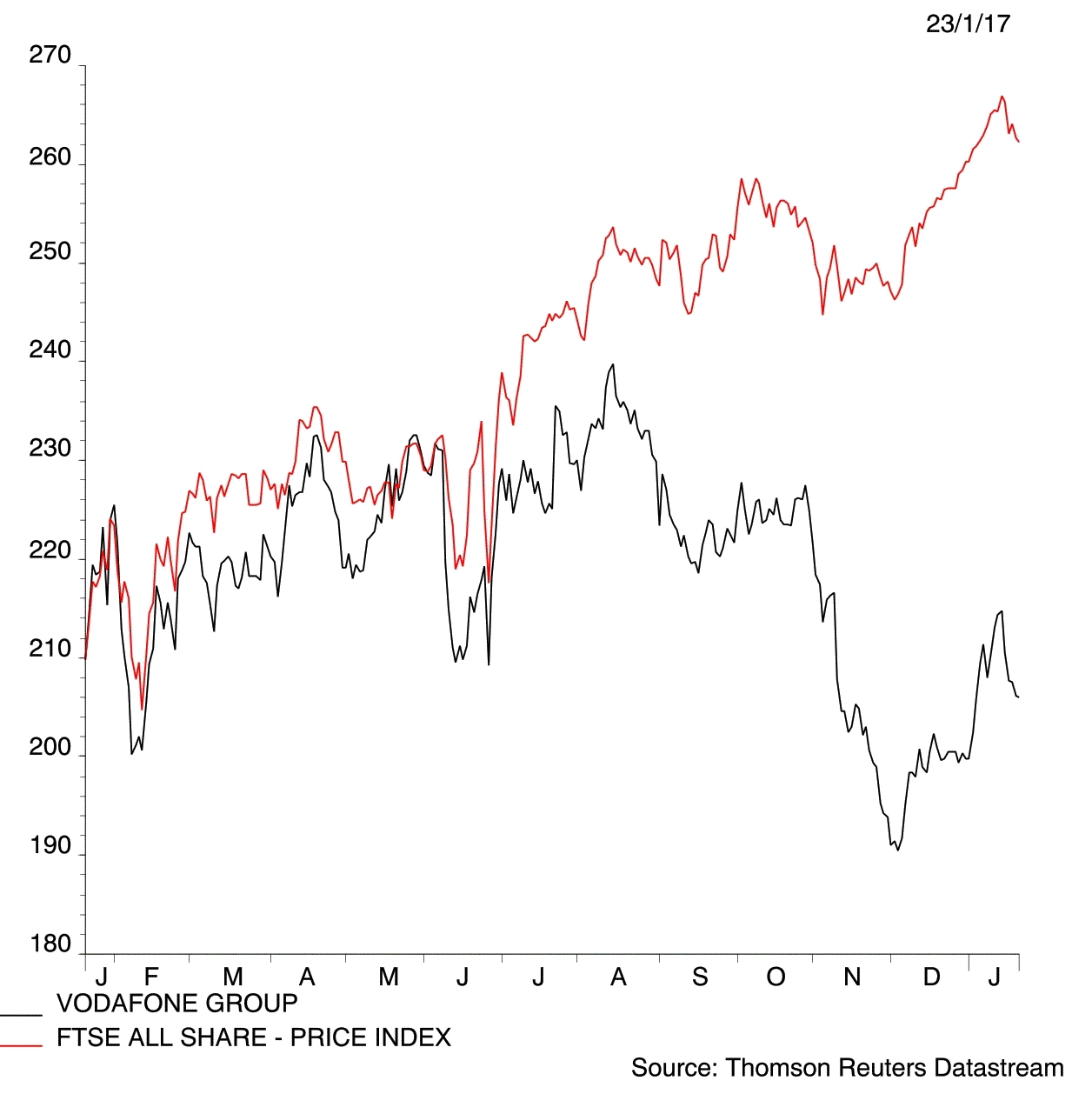

Some City number crunchers believe that there is a substantial 33% upside on the table for shareholders this year. The stock currently changes hands for 205.85p.

Vodafone is one of Europe’s largest mobile operators, with operations in the UK, Germany, Italy and Spain, plus India, South Africa, parts of the Middle East and Asia Pacific. It is also one of the most frequently traded stocks, with upwards of 40m shares regularly changing hands on a daily basis.

Dividend debate

The £54bn group is emerging from a period of heavy capital investment, otherwise known as Project Spring, which has constrained earnings and made its dividend cover look particularly skinny.

According to Reuters data, the consensus of analyst forecasts for the mobile group stands at €0.15 per share for the full year to 31 March 2017, or about 12.9p per share at the current 0.862 euro/sterling conversion rate. Earnings per share (EPS) for the same year is pitched at less than half that amount, €0.07 (6.1p).

If those estimates prove right this year will be the third in a row that EPS has failed to cover the dividend, with borrowings used to support the payout.

The market’s current view of the group’s prospects means that this situation could persist for several years, meaning little or no growth in income for shareholders.

Market too negative

But future prospects may not be anything like as bleak as they may appear. One source of encouragement came in interim results to 30 September, when Vodafone raised its half year dividend by 1.9% to 4.74c, or about 4.1p.

The main message from those results was of improving strength across much of Europe offsetting a decline in the UK, although even here the rate of reverse is slowing.

Since those results a growing army of City brokers and investment banks have highlighted what they see as over-played challenges for Vodafone, with precious little credit given for potential positive surprises. This growing weight of opinion includes analysts at Jefferies, Berenberg and UBS.

Previously troubled markets, such as Italy and Spain, are showing convincing signs of improved operating metrics.

‘The Italian unit is looking to accelerate cost saving measures going forward,’ say UBS analysts Polo Tang and Michael Hill, who also flag strong growth in fixed line in the region.

In Spain, UBS reckons Vodafone can increase its 20% market share within the low cost segment. ‘We see scope for Vodafone to more actively promote its Lowi mobile brand in the value segment and start offering a no-frills converged fixed/mobile bundle,’ the pair say.

European outperformance

This implies that Vodafone’s European operations may be capable of doing substantially better than the zero to low single-digit revenue and EBITDA (earnings before interest, tax, depreciation and amortisation) growth forecast for the next few years, after eight years of decline.

India has been a particularly fast moving mobile market, and troubling for Vodafone. It was recently forced to write-down its Indian business by £4.3bn. Adding to the pressure is Reliance Industries (RELI:NS)-backed Jio, which has been controversially providing all mobile services for free since its mass launch in September, a promotion that Vodafone and others have labelled anti-competitive.

Reliance reaffirmed its commitment to ongoing free Jio mobile services for the foreseeable future on 13 January.

This has prompted speculation of telecoms consolidation in India in which Vodafone would likely be a lead player. This could potentially kill two birds with one stone; addressing competition and increasing market share in this multi-billion pound market.

M&A boost

Merger and acquisition (M&A) activity could provide positive catalysts elsewhere, a combination with Liberty Global (LBTYA:NDQ), the owner of Virgin Media, has often been mooted.

A merger was recently completed between their respective Dutch assets. ‘We see a broader deal between the two as a value-accretive step,’ explain UBS’s Tang and Hill, a point on which Berenberg analysts agree. ‘The move would create a leading converged fixed/mobile

operator in Europe and potentially realise significant synergies.’

In addition, Vodafone should benefit from rising 4G penetration, growing mobile data usage, recent ‘more-for-more’ price changes and growth in fixed line services.

‘We think recovery and operational gearing have been underestimated with the shares implying no top-line growth. We also see M&A upside potential from a broader deal with Liberty Global,’ concludes UBS.

We agree that the market is too gloomy over Vodafone as a whole and dividends in particular. The current above sector average income yield of 6.3% remains attractive.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.