Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy or sell: What to do when a share price falls

Buy low and sell high. Sounds simple, doesn’t it? Investors following this advice have over the years become either extremely rich or flat broke.

So when should investors buy after a big market fall?

The challenge is deciding whether or not to top up on an existing holding without risking too much money on one stock or fund. You may need to make a tough decision and exit the investment, potentially at a loss.

How to approach the situation

We explore in this article the different ways to weigh up the situation when your investment has declined in value.

We explain how to consider the evidence in terms of trading or financial strength, as well as market sentiment.

Furthermore, we look at three stocks in detail where investors are currently deciding whether they should buy on share price weakness or avoid ‘catching a falling knife’. These are cake maker Premier Foods (PFD), invoice finance group Tungsten (TUNG:AIM) and platinum miner Lonmin (LMI).

How to avoid losing money

John Hempton, chief investment officer at Australian hedge fund Bronte Capital, recently sought to answer one of the most difficult questions investors face.

Hempton’s advice is wise: ‘Be careful’.

Averaging down is a process where investors buy more shares in a company or units of a fund they have already invested in after a price decline. This can quickly become extremely costly to a portfolio if a price keeps falling.

‘Averaging down has been the destroyer of many a value investor,’ writes Hempton on Bronte Capital’s highly informative blog.

‘Indeed averaging down is the iconic way in which value investors destroy themselves and their clients. After all, if you loved something at $40 a share and you were wrong, you might love it more at $25... and like it more still at $12. And you could be equally wrong.

‘And before you know it you have doubled down three times, turning a 7% position [in your portfolio] into an 18% loss.’

He says you could easily be down 50% on your investment by averaging down on a few stocks. That could balloon to an 80% loss in a bad market, adds Hempton.

‘And if you do not believe me, this has a name: (former Legg Mason fund manager) Bill Miller,’ he states. ‘Bill Miller assembled a startling record beating the S&P 500 every year for 15 straight years. And then it blew up.

‘Miller had a (false) reputation as one of the greatest value investors of all time: he is one of the biggest stock market losers of all time and a model of how not to behave in markets,’ claims Hempton.

‘How not to behave is to be a false value investor, buying stocks on which you are wrong and recklessly and repeatedly averaging down,’ he adds.

How to average down

Hempton cites the example of Paul Tudor Jones, a US hedge fund manager who made his name by predicting the 1987 Wall Street Crash. This investor took a completely opposite approach to Miller.

Tudor Jones used to have a poster on his office wall that read ‘Losers Average Losers’, referring to the idea that averaging down was more likely to lose money than make money.

Is there a middle way between these two extremes?

Warren Buffett’s approach to investment may offer some clues. The Berkshire Hathaway chairman says he is happy when stocks he is buying fall in value – it allows investors to buy the same number of shares at a lower price.

But that’s because Buffett approaches buying a stock in the same way as he approaches buying anything else: whether it is an entire business – or even a hamburger.

‘When the price of hamburgers goes down there is joy in the Buffett household,’ Buffett says.

‘We eat well. When the price goes up, we don’t buy so many. What is different about shares?’

Averaging down example: Capita

Buffett’s whimsical comments contain an important insight: shares are a reflection of a company’s market value.

Investing in the stock market in the same way as you would if you were buying an entire business can change the perception of risk.

Let’s take an example of how this works: Capita (CPI) is a good one after its share price plunged from £13.20 in the middle of 2015 to 507p a share after a string of profit warnings in 2016.

Are shares in Capita riskier now than they were 12 months ago?

Investors who focus on Capita’s share price might well say ‘yes’ – with justification. There are clear risks to the company’s profitability and chief executive Andy Parker has said the UK’s vote to leave the EU is a major headwind to the company.

Others highlight the company may need a rights issue to reduce its debt and Capita is also selling off profitable businesses to improve its balance sheet.

Clearly, Capita’s share price could fall a lot further if more problems are identified.

Is Capita more or less risky after big price declines?

Now let’s think how a private equity company or commercial rival might consider the risks and opportunity of an investment in Capita via a takeover. The question of risk becomes very different.

Capita’s market value before its numerous profit warnings was £8.8bn at £13.20 a share. Today, its market value is £3.4bn.

By definition, it is less risky to buy all of Capita at £3.4bn than it is to pay £8.8bn: the buyer is risking less capital.

A company with £8.8bn to spend on acquisitions can now afford to buy Capita plus another business, if it so wished.

So how can investors make this different thinking work to their advantage?

One method – and investors should be clear that this is an unconventional approach – could be to scale positions in a portfolio along similar lines.

The approach is intuitive in a sense: invest smaller amounts in riskier stocks and larger amounts in less risky companies.

Two sides of the coin

A falling share price can suggest something is wrong with a company. If true, can the problem be fixed?

Share price weakness can also make the same company more attractive to a takeover bid. But is it worth buying, even at a lower price?

Turn volatility to your advantage

Let’s take the example of an investor with a £100,000 equity portfolio who invests across 20 stocks with an average invested in each stock at £5,000.

If you normally invest around £5,000 in each stock and are considering investing in Capita, why not turn the lower share price to your advantage?

Capita’s shares are down around 60% since 2015. One option could be to open a position that is 60% lower than your average, in this example around £2,000 and holding the rest of your cash in reserve or investing it in something else.

This would mean buying 394 shares in Capita – the same number you would have bought at £13.20 a share, but paying 60% less.

Now let’s see what happens if Capita’s share price falls again. If the stock price halves down to say 250p, it only costs £985 to buy another 394 shares.

And if it halves again, to 125p, it would only cost £493. Averaging down in this way, an investor keeps some of the upside but avoids overexposing themselves on the downside to one particular stock.

Even at this point, the maximum the investor could lose is £3,478, less than 5% of their entire portfolio.

Set limits

Hedge fund manager Hempton at Bronte uses a similar approach. Each time a new stock is added to the Bronte portfolio, Hempton sets a maximum loss limit on each position. He makes the positions smaller on stocks which look riskier.

‘The default at Bronte is that we have set the maximum percentage for a stock, typically 9% [of the portfolio] but often as low as 3% depending on how we assess the risk of the stock,’ writes Hempton.

‘As fund manager, I am allowed to spend that whenever I want but I am not allowed to overspend it. If we have a 6% [of the portfolio] position with a 9% loss limit and it halves, I am allowed to add three percentage points more to the exposure. But that is it.’

Measure your risk in pounds

The key point is this: Investors that want to take advantage of falling prices should do so very conservatively. You should avoid becoming heavily overinvested in individual stocks or funds.

Investors who really like to buy as prices fall could consider the aforementioned approach: buying the same number of shares at lower and lower prices – while always ensuring the total amount of capital at risk is less than or in line with other positions in your portfolio.

Hedge fund manager Hempton also argues that companies which have a lot of debt are generally best to avoid averaging down on.

As Hempton says, don’t let a 7% position in your portfolio lose 18% of your portfolio’s value. But equally, don’t be put off making a sometimes irrational stock market work to your advantage.

Checklist if you are considering buying when a share price has fallen

1. Why has the share price fallen? – is the problem linked to fears over inability to service debt, trading problems, accounting scandal, negative market backdrop, large investors selling chunks of shares?

These are some examples of factors that can weigh on a share price. A stock can be cheap; yet it can be cheap for a negative reason which means lower share prices do not always equate to being bargains.

You need to be able to identify how the company can fix problems and address the factors preventing its share price from rising.

2. If you cannot see a catalyst for fixing any problem, how can you

be certain the share price will stop falling?

3. The optimal situation for value investors is to spot a stock where the market has incorrectly priced in certain risks that won’t actually manifest into real problems. ‘The market has got it wrong’ is the best way of summarising this situation. It isn’t easy to find stocks which fit the criteria; but it is certainly not impossible.

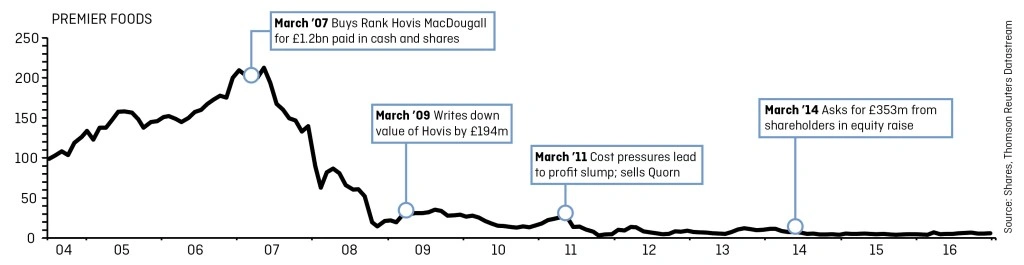

Premier Foods (PFD) 41p

Food manufacturer and Mr Kipling brand owner Premier Foods has been a perpetually falling knife for the past decade.

Premier has become a ‘zombie’ company, according to Shore Capital analyst Darren Shirley, a term used to describe companies with no economic value that continue to survive via cheap loans.

That’s a bit unfair, in our view. While our retail expert James Crux has had a consistently bearish, and consistently correct, stance on Premier’s stock for many years, the company is not a poor business: it simply has an inappropriate financial structure. There’s a big difference.

Why Premier is still worth a look

Premier’s core business is impressive. It has 17% operating margins and its return on tangible assets is 14%, much better than the average company on the stock market.

It also operates in relatively defensive markets. Premier’s problems revolve around its debt load which is £556m, some four times trading profit. It also has a pension deficit of £183m.

Add these liabilities together along with Premier Foods’ market capitalisation of £356m and you get an enterprise value of £1.1bn versus year-ahead trading profit estimates of £118m.

A company of Premier’s quality would trade at an equity value far in excess of £1.1bn if its debt and balance sheet liabilities were extinguished, in our view.

Comparisons across the industry provide a less bullish perspective.

Smaller rival Finsbury Food (FIF:AIM), for example, trades at an enterprise value to operating profit of 10.2. On this basis, Premier Foods is only a little cheaper at 9.3 times the same ratio.

Still, Premier’s margins are triple those at Finsbury and it boasts a stable of attractive brands including Oxo and Ambrosia.

There is a lot to like about the business, in our view, but investors really need to do their homework on how much additional equity they would be willing to invest in this business via a potential rights issue, if needed.

Tungsten (TUNG:AIM) 64p

Loss-making invoice discounter Tungsten has tumbled from highs of over 400p a share to 64p amid slower-than-expected progress on reaching break-even as well as board room angst.

Financier Edi Truell persuaded a constellation of high flying City bakers including Icap founder Michael Spencer to back Tungsten’s IPO in 2013 at 225p a share.

Truell’s pitch was simple: use the shift from paper to electronic invoicing to create a vehicle which not only automates the processing of invoices but also provides companies with new financing options.

Companies, after they have sold their products, want to turn invoices into cash as quickly as possible. Equally, investors are very keen to lend against the ‘promises to pay’ which they represent.

Making these transactions electronic not only improves administrative efficiency, it makes them much simpler to turn into financing agreements.

How does invoice financing work?

• Sainsbury’s buys a batch of Mr Kipling cakes from supplier Premier Foods

• Premier Foods ships the product and sends an invoice to Sainsbury’s

• Sainsbury’s approves the invoice and says it will pay within 30 days

At this point, investors can buy this approved invoice from Premier Foods at a slight discount to the amount which will be paid from Sainsbury’s. This gives Premier Foods immediate access to the cash, minus a small discount. Sainsbury’s pays the cash straight to the investors rather than Premier Foods.

In this way, an invoice has been turned into an interest-bearing financing instrument.

While it sounds great in theory, progress at Tungsten has been slower than expected.

Spencer, who backed the IPO, left Tungsten’s board and is said to have fallen out with Truell.

Then Truell also left the company, leaving it the hands of current chief executive Richard Hurwitz.

Tungsten now aims to hit monthly break-even sometime in the calendar year 2017.

It is also starting to see uptake in the financing product, which it says will start generating ‘material increases’ in revenue during its financial year ending in April 2018.

Patient investors could be rewarded handsomely if Hurwitz delivers on these initiatives.

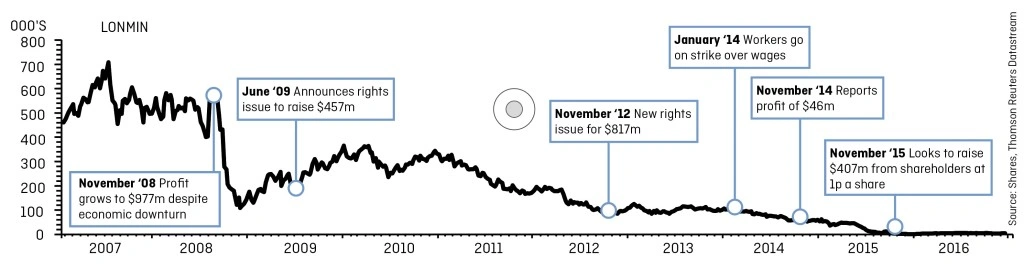

Lomin (LMI) 170p

Former FTSE 100 platinum miner Lonmin’s fall from grace represents a stark warning for any investor thinking of averaging down on a falling share price.

Struggling companies can fall a long way quickly. Add a highly dilutive rights issue on top and you have a recipe for savage declines in shareholder value.

Shortly after Lonmin shares hit their all-time high in 2006, the South Africa-based mining company announced results which showed operating profit of $842m and net debt of $458m.

As the prices of precious metals started to weaken in the late 2000s, profit began to decline. Since 2009 Lonmin has run into a range of problems including strike action from employees which have seen it swing between small profits and heavy losses, racking up debt in the process.

Lonmin raised equity from shareholders for the first time in 2012, tapping up investors for $817m. It did the same again in 2015, asking for $407m via a 46 for one rights issue at 1p a share.

By the 2015 equity raise Lonmin was considered by investors to be virtually worthless. It was only the backing of South African state investment fund Public Investment Corporation which allowed it to raise sufficient money to survive.

Even after raising more than $1.2bn from shareholders over the last four years, Lonmin is valued on the London market at just £486m.

Regardless of your strategy around averaging down, there’s no way to make money from a company which burns through shareholder capital and a stock price which drops like a stone.

Didn't mining equities surge last year?

Lonmin has returned to form more recently on the back of a rebound in commodity prices: its shares have more than quadrupled in the past year.

The commodities price rally still only helped the business register a break-even result in the year to 30 September 2016. Guidance for platinum output in the year ahead is lower than that achieved in the previous 12 months.

Optimists might see valuation upside if Lonmin can put its chequered recent past behind it.

Set up in 1909, Lonmin has a distinguished longer-term track record. Even after its recent troubles, the shares have delivered a total return of almost 7% annualised over the past half century. Admittedly most Shares readers won’t have held the stock for 50 years.

But for a turnaround that is now more than a decade old and counting, Lonmin investors will need deep pockets if more equity is required.

There are also increased risks now a state-backed investment vehicle owns 29.9% of the company’s shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.