Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTop fund ideas to bolster your ISA in 2017

Here are six ideas from the funds space to give your portfolio a healthy New Year boost. They can help to diversify your portfolio as you can access multiple companies or other assets via single products. We’ve also added another idea as a fund to watch.

While our main feature this week looks at stocks to add to your ISA, we appreciate that not everyone wants the risk of buying individual companies.

That may certainly be the case for investors who want to buy something and forget about it. The beauty of funds is that a fund manager is paid to do the hard work of checking the underlying assets remain suitable, leaving you free to get on with your life.

All the ideas have come from financial service group Winterflood’s top picks in the closed-ended funds space for 2017. We’ve selected six investment trusts from its list including some of the main geographic areas and a specific income-themed product.

WOODFORD PATIENT CAPITAL (WPCT) 93p

The brainchild of one of Britain’s most famous fund managers Neil Woodford, the investment trust’s objective is to achieve long-term capital growth in excess of 10% per year through a portfolio of UK companies in the main, split between quoted and unquoted names.

Admittedly the fund hasn’t hit this goal since launching in April 2015. It is still very early days and the clue is in the name – this is a fund for ‘patient’ investors.

Woodford is financing companies that offer significant potential upside, typically through their intellectual property.

‘The fund is not a mainstream play on UK equities; however, we believe that it offers attractive exposure to secular growth,’ says Winterflood.

‘In our opinion the strategy of Woodford Patient Capital is a natural extension of the investment approach that Neil Woodford has honed over a number of years. He has already backed numerous public and private early-stage and early-growth companies on the basis of significant upside potential and he believes that a lack of financing for these companies offers a valuation opportunity.’

There is no annual management fee. Instead, the fund charges a performance fee of 15% of any excess returns over a 10% per year cumulative hurdle.

In the first half of 2016, holdings in larger companies including GlaxoSmithKline (GSK), AstraZeneca (AZN) and Legal & General (LGEN) were sold, with proceeds reinvested into existing smaller quoted company positions trading at lowly valuations.

Currently, the largest holding in a portfolio dominated by healthcare and financials is biotechnology company Prothena (PRTA:NDQ).

Other holdings include unquoted pair Immunocore and Oxford Nanopore, 4D Pharma (DDDD:AIM), online hybrid estate agency Purplebricks (PURP:AIM) and biopharmaceutical play Mereo BioPharma (MPH:AIM).

TEMPLE BAR INVESTMENT TRUST (TMPL) £12.44

Winterflood likes investment trust Temple Bar for its good long-term performance record available at a ‘slightly wider discount’ to net asset value than the peer group weighted average.

The portfolio manager Alastair Mundy has been in place since November 2002 and adopts a contrarian approach to investing. This involves buying companies on the FTSE 350 index which have at least halved from their peaks but which have reasonable balance sheets.

Stocks are then held for around four to five years to allow time for the companies to turn around.

This investment strategy makes periods of underperformance almost inevitable but, as the Winterflood team note, ‘there is much merit in Alastair Mundy’s contrarian approach, particularly for long-term investors’.

Making a decision on whether or not to invest probably requires you to take a view on the banking sector as four UK banks feature in the top 10 holdings.

MONKS INVESTMENT TRUST (MNKS) 608p

Monks is a good selection for anyone wanting exposure to international equities. It is very much a growth-focused fund albeit containing many well-established businesses. ‘The managers are prepared to “embrace the asymmetry of returns” recognising that the upside on any investment is theoretically limitless, while the downside is limited to how much you put in,’ says Winterflood.

The top 10 holdings include two well-known UK-listed stocks, being insurer Prudential (PRU) and construction group CRH (CRH). These are complemented by the likes of Amazon (AMZN:NDQ), Royal Caribbean Cruises (RCL:NYSE) and American banking-to-wealth management group First Republic Bank (FRC:NYSE).

The investment trust’s charges are low at 0.59% and it benefits from a well-resourced management team in the form of Baillie Gifford. Monks has delivered 97.5% share price total return over the past five years. That’s slightly behind its benchmark; however, Monks switched to Baillie Gifford’s successful Global Alpha Strategy in 2015 so there are hopes that performance statistics will soon start to look better.

BAILLIE GIFFORD JAPAN (BGFD) 604.75p

It’s been called the stand-out performer within the Japan sector by analysts, and there’s no doubt that both share price and net asset value returns command respect.

The investment trust has substantially beaten its benchmark Tokyo Stock Exchange Price Index over 10, five and three years, although that’s evened out over the past 12 months.

Perhaps this is a reflection of money flows into larger Japanese companies versus the trust’s small and mid-sized focus. The one exception is telco-to-technology group Softbank (9984:T) which is the trust’s biggest holding and new owner of UK microchip design firm ARM.

Major themes include ‘internet everywhere’, global industrialisation and franchise value creation. That implies a hefty interest in engineering and electronics, among other things.

With a team of eight scouring the nation for investment opportunities, it typically holds between 40 and 70 stocks and turnover is reassuringly low, suggesting good initial analysis and capping trading costs.

FIDELITY EUROPEAN VALUES (FEV) 190p

Investors seeking exposure to Europe should prioritise companies with progressive dividends, rather than high growth stocks, as these could outperform over time.

One investment trust that adheres to this approach is Fidelity European Values. It seeks to achieve long-term capital growth principally from the stock markets of continental Europe. It trades at nearly 12% discount to net asset value.

Manager Sam Morse follows three key investing principles. First is a bottom-up stock selection with a focus on dividend growth. He takes a long-term view which improves performance and reduces costs.

Morse also has a cautious approach, stemming from his belief that managing downside risk creates a strong foundation for long-term outperformance. Morse invests in companies based on their prospects for producing dividends and dividend growth as this indicates steady structural growth.

Its portfolio positions include food giant Nestle (NESN:SWX), cosmetics colossus L’Oreal (OREP:PA), healthcare company Novo-Nordisk (NOVOB:CO) and Helsinki-listed insurer Sampo (SAMPO:HE).

TEMPLETON EMERGING MARKETS (TEM) 620.14p

The lingering discount to net asset value in the region of 10% at Templeton Emerging Markets is unjustified according to Winterflood, given lead manager Carlos Hardenberg’s success in reversing historically weak performance.

Since he took over in October 2015 the fund has delivered a net asset value total return of 56% against 40% from the benchmark.

Winterflood sees the discount as a ‘notable value opportunity’ and notes it enjoys ‘superior liquidity’ over rivals because it is by far the largest investment trust in its peer group.

We think this fund could be a good place to start if you want exposure to emerging markets.

Hardenberg has increased diversification with the number of holdings hitting 96 as at 30 September 2016 compared with 56 a year earlier. He has also significantly increased exposure to information technology stocks, with Samsung Electronics (005930:KRX) and Taiwan Semiconductor Manufacturing (2330:TPE) among the top holdings.

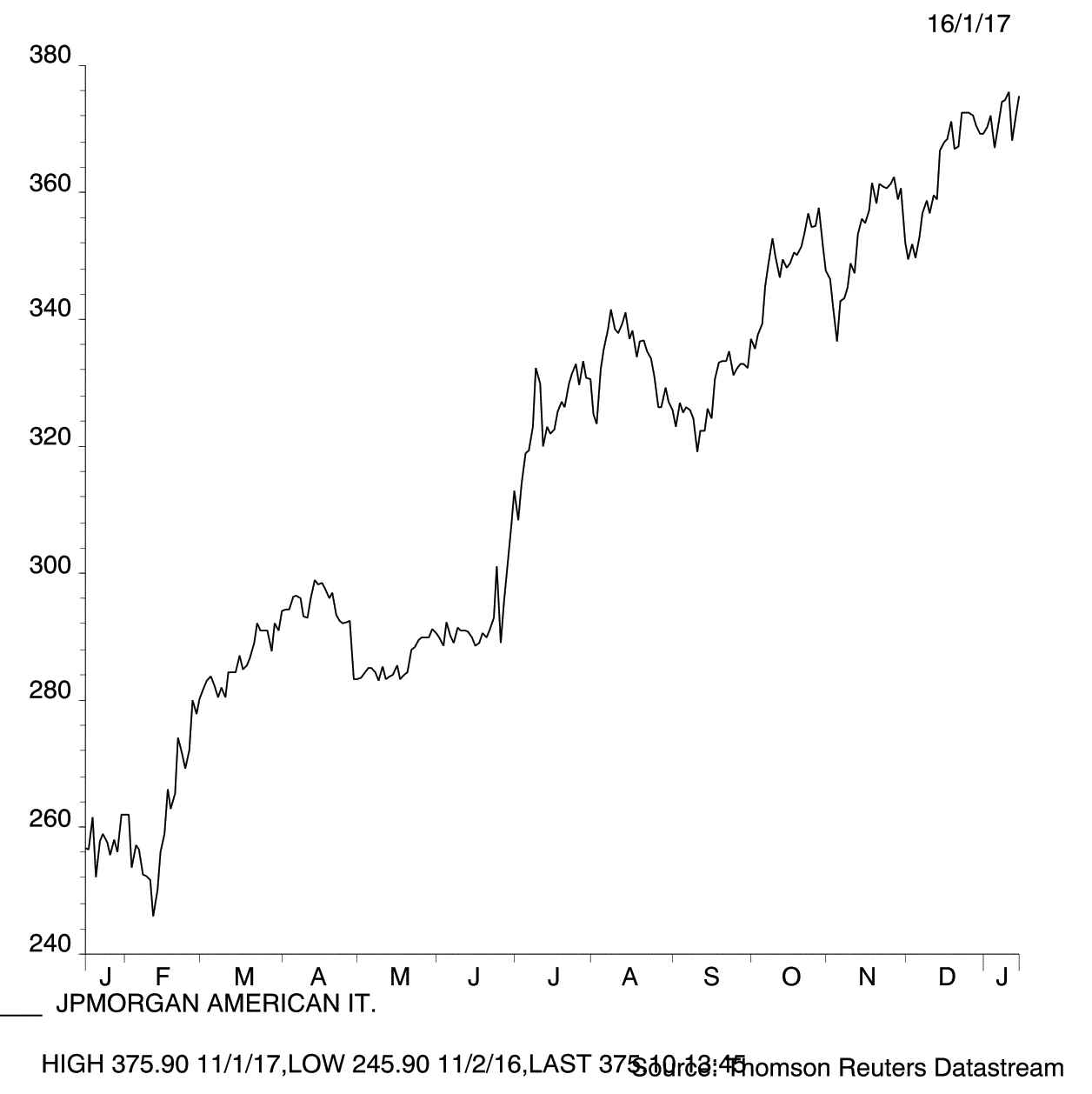

JPMORGAN AMERICAN (JAM) 375.1p

This US equities fund mainly invests in large cap firms exposed to long-run growth drivers.

However, the fund hasn’t outperformed its S&P 500 benchmark over the past 10 years. Winterflood is confident the fund is still worth buying as it highly rates fund manager Garrett Fish.

Ongoing charges of 0.62% are fairly cheap for an actively-managed fund – but you could potentially get an even-cheaper exchange traded product that tracks the S&P 500 and delivers a similar performance. For that reason, we put the fund on our watch list until Fish ups his game.

Technology and healthcare are key themes among the fund’s holdings which include Apple (AAPL:NDQ) and Gilead Sciences (GILD:NDQ).

The bigger company component is managed by long-term manager Garrett Fish but there’s also approximately 6% of the fund in smaller US stocks, run by Eytan Shapiro.

It trades on 2% discount to net asset value. It has often traded at a premium in the past. The scale of any discount is also presumably capped thanks to the fund’s active share buyback scheme.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.