Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineQuality insurance arm to revive Personal Group

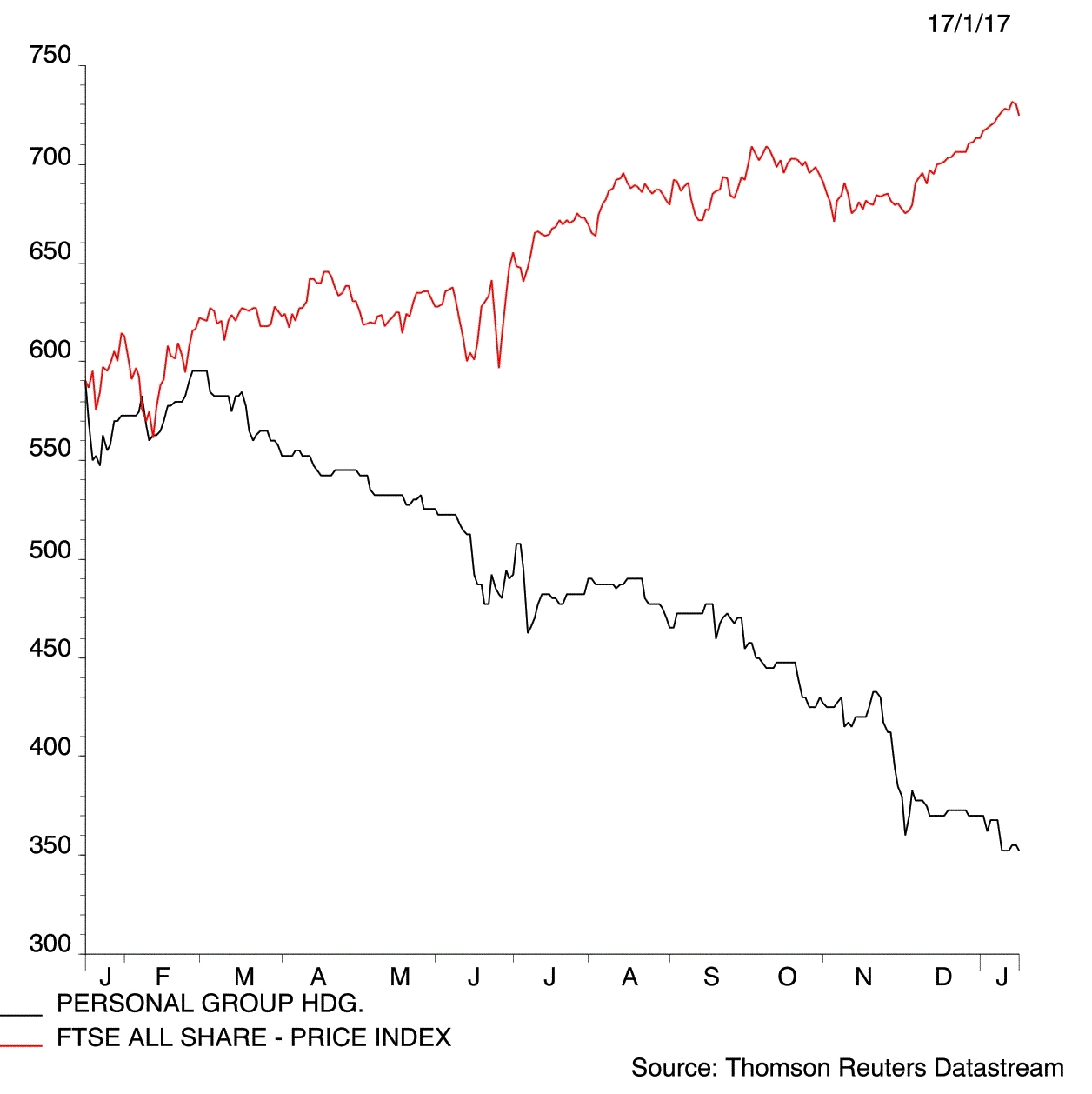

A sell-off at insurance and employee benefits specialist Personal Group (PGH:AIM) may offer an opportunity to pick up shares in a good company at a reasonable price.

Personal Group’s share price has been under pressure because of weak performance in its non-insurance business, in part because of government changes to rules on staff perks.

While these will weigh on performance in the near-term, Personal Group has a small but high quality insurance business which offers longer term growth via a tie-up with payroll giant Sage (SGE).

Profitable insurer

Insurance is expected to deliver pre-tax profit of close to £10m a year for the next three years – though there may be a dip in 2016 because of an increase in operating costs. Personal Group’s key insurance products are hospital and convalescence plans and death benefits provided by employers for employees.

For investors to get really excited about Personal Group, however, it needs to start generating growth in its non-insurance divisions, which have been losing money in recent years.

Personal Group offers a range of employee benefits packages to small and medium firms.

The most promising product is its mobile app-based employee benefits package Hapi. Offering a service that allows SMEs to provide employee benefits comparable to those offered by larger organisations, it should be profitable in its own right as well as providing a new distribution channel for insurance products.

The package is being offered through a partnership with Sage, whose enormous client roster should expand the insurance product’s reach in the UK and Ireland.

A trading update published on 10 January revealed Personal Group delivered earnings before interest, tax, depreciation and amortisation (EBITDA) marginally ahead of expectations in 2016.

Profit guidance had already been reduced earlier in the year, meaning earnings per share (EPS) for 2016 is expected to decline from 27.2p in 2015 to 21.9p.

Scanlon still expects EPS to grow in 2017 though earnings will not be as high as the 34.5p previously forecast by analysts.

Risks to consider

Key risks include a failure to deliver growth via the Hapi app, a downturn in performance in the insurance division, or unexpected losses in the company’s other divisions.

While these risks are not to be taken lightly, Personal Group looks set to return to growth in 2017, in our view, and could continue to grow for many years.

Personal Group (PGH:AIM) 350p

Stop loss: 276p

Market value: £107m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.