Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWere you lucky to own shares in the star performers?

MARKET CAP £1bn and above

ANGLO AMERICAN +287%

Few people would have predicted a year ago that 2016’s best large cap performers on the stock market would be mining stocks. Fast forward a year and the evidence is clear – eight of the top 10 top risers are commodity producers.

Anglo American (AAL) was one of the most heavily-shorted stocks in 2015 amid concerns about its huge debt pile and poor business prospects. In January 2016 it was the fourth smallest company in the FTSE 100 and faced demotion from the blue chip index.

So how did its shares manage to subsequently rise 287%? Commodity prices rallied, helping to improve its earnings and put the company in a better position to service its debt. We have a favourable view on the mining sector but see better opportunities elsewhere, such as Rio Tinto (RIO), Kaz Minerals (KAZ) or BHP Billiton (BLT) among the larger businesses.

SOUTH32 +201%

Lower down the market spectrum, albeit still valued at more than £1bn is South32 (S32). This is the coal and manganese business spun out of BHP in 2015. Its 201% gain year to date is down to the surprise rally in coal prices.

It has enjoyed significant earnings upgrades and generated bucket loads of cash. It reduced net debt by $714m in the past financial year and ended up with a $312m net cash position.

South32’s future seems to lie in metallurgical coal which is used in steel making and which sells for a higher price than power generation product thermal coal.

We find it hard to get too excited by the broader coal sector because of uncertainties over demand. Our cautious stance is chiefly linked to climate concerns around the world. We think the coal price rally has hit, or is near to, its peak and we prefer other commodities such as copper and oil.

South32 certainly looks interesting at present but we certainly don’t expect such a good performance again in 2017 from its share price. Chinese coking coal stockpiles (according to reported figures) are at their highest level since February 2015 and Chinese supply availability is improving, says investment bank Macquarie.

Commenting on the broader mining space, Macquarie last week made a fascinating remark about the sector which investors would be wise to consider.

It said: ‘The current period marks a window of opportunity for resource producers, with commodities trading out the cost curve and costs themselves not rising – indeed, we are in the free cash flow sweet spot at present. Meanwhile, everything that has been helping commodity markets over the past six months will likely still be true for the next six. However, such periods don’t last forever.’

BOOHOO.COM +268%

After a wobbly start to the life on the stock market, online fashion retailer Boohoo.com (BOO:AIM) spent 2015 in recovery mode and then raced ahead in 2016.

It enjoyed a flurry of earnings upgrades driven by stellar growth delivered at home and abroad.

Investors chased the shares higher following the EU referendum too; keen to harness Boohoo’s international growth potential and status as a currency winner. Sales generated overseas are worth more on translation into sterling.

We remain fans of the structurally-advantaged fast fashion seller. Boohoo’s dedication to own brand product supports high margins, while a ‘test-and-repeat’ model limits fashion risk.

Most low-cost retailers source their clothes from low-cost producing countries and typically have to place a large order to make it cost efficient to import.

Approximately 80% of Boohoo’s clothes are sourced from UK manufacturers. The company can get a small run of clothing very quickly.

A big order is placed if clothes from that small run sell ok, otherwise it scraps the product. It means Boohoo doesn’t have the stock obsolescence problem strangling other retailers.

Strongly cash generative and boasting a brand that is increasingly popular with the youthful web-savvy demographic, Boohoo’s acquisition (14 Dec) of a 66% stake in PrettyLittleThing is a highly complementary deal that will further augment its already enviable growth rates.

BURFORD CAPITAL +195%

Litigation funder Burford Capital (BUR:AIM) rounded off 2016 in style, sealing the $160m (£126m) acquisition of rival Gerchen Keller. Burford has this year impressed investors with its ability to deliver strong returns from funding commercial litigation claims.

Burford’s success since listing in 2009 at 100p a share has gone a long way towards proving the attractiveness of litigation finance. It now trades at 576.5p.

Chief executive and founder Christopher Bogart led the business to a 28% gain in book value after adjusting for dividend payments, Shares’ preferred measure of performance for Burford, in the six months to 30 June. Book value at $492m compares with a current market capitalisation of £1.1bn.

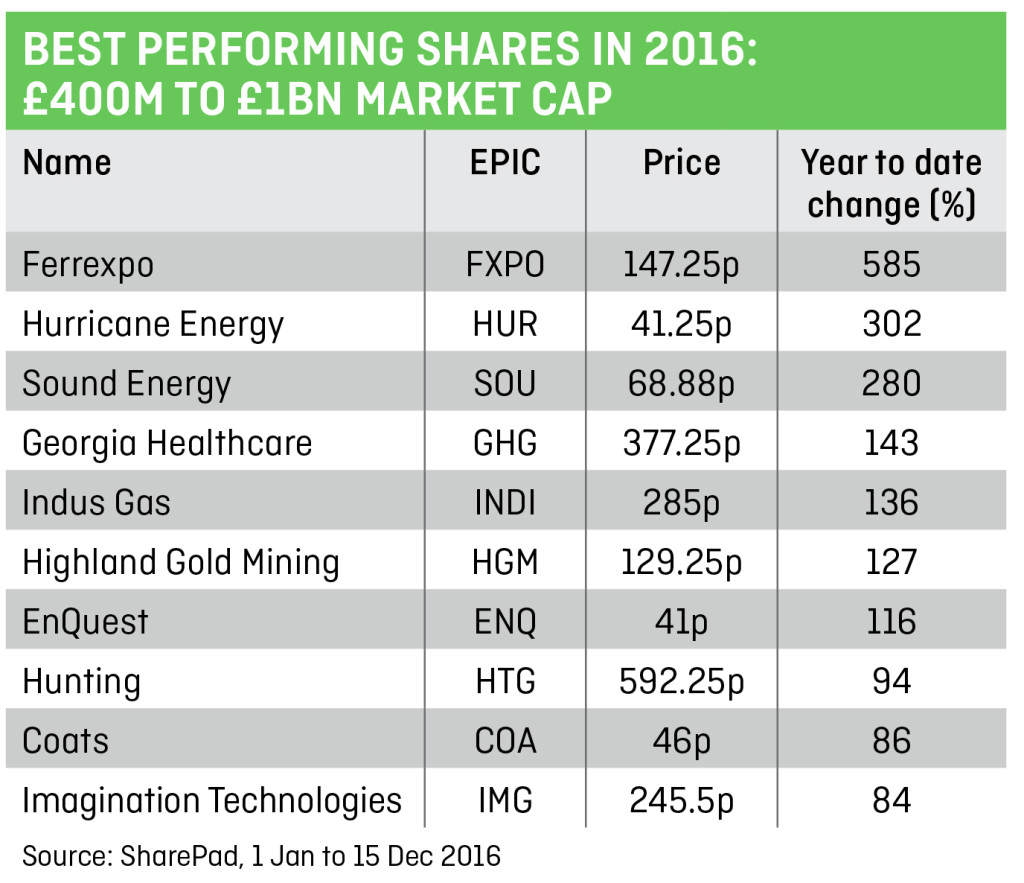

MARKET CAP £400m to £1bn

HURRICANE ENERGY +302%

The ability of Hurricane Energy (HUR:AIM) to raise cash at a premium in 2016 is testament to the excitement its story has generated in the market.

The £52.1m placing in April enabled the company to drill an appraisal on its Lancaster discovery and in September the highly encouraging results of this well helped light a fire under the share price. This supported a subsequent £70m fundraise.

Drilling activity should be able to sustain the momentum behind the share price. Hurricane is targeting fractured basement reservoirs, a largely untapped source of hydrocarbons in the UK which has been exploited in Yemen, Libya and Vietnam.

ENQUEST +116%

North Sea oil producer EnQuest’s (ENQ) position among the top performers reflects some operational progress but also the company’s leverage to oil prices and a recovery from an extremely low base.

Despite some weakness following the US Federal Reserve’s decision to raise interest rates (14 Dec), the price of oil is still almost double its 2016 low of £27.10 seen in late January.

EnQuest loaded up on debt when oil was at $100 per barrel. As a result even the slightest movement in crude can have a significant impact on earnings-linked debt covenants. Although we are broadly positive on oil in 2016, EnQuest remains a high risk play thanks to its borrowings and we see better opportunities elsewhere.

COATS +86%

‘Industrial threads specialist Coats (COA), one of the original constituents of the FT30 in 1935, is another piece of British corporate history which we believe could attract interest in time.’ We wrote that line in July 2015 when the shares traded at 25.2p. They now change hands for 46p.

Coats used to be part of conglomerate/asset manager Guinness Peat. The latter divested its assets and investments to eventually be left

with Coats.

The market did indeed pick up on the stock’s attraction, hence the 86% gain in 2016. We think there is much further to come from the shares and view it as an attractive investment.

‘Coats is a profitable, highly cash generative, global market leader in industrial threads and specialty fibres, emerging from complex recent history,’ says Canaccord Genuity analyst Casper Trenchard.

‘In our view, likely resolution of the pension issues is the key threshold, enabling the company to leverage its net cash balance sheet via the introduction of a progressive dividend policy (including potentially special capital returns) and a more concerted, and accretive, acquisition strategy. Entry to the FTSE Mid-250 potentially beckons in 2H17, further expanding its appeal to investors.’

MARKET CAP £100m to £400m

SOLGOLD +1,060%

AIM-quoted SolGold (SOLG:AIM) told the world in 2010 that it had a world class exploration discovery, prompting the share price to increase nearly nine-fold in a few days.

While we didn’t like the way in which it went about hyping the asset, the company had the last laugh this year after it was on the receiving end of a bidding war by two of the world’s biggest miners eager to invest in the company.

SolGold’s share price had progressively fallen since the initial hype in 2010 surrounding its Cascabel copper deposit in Ecuador. A mix of commodity price recovery and renewed interest from majors in backing growth projects has this year resulted in a massive u-turn for the equity.

BHP Billiton saw its $30m offer to buy a 10% stake in SolGold rejected in favour of NewcrestMining (NCM:ASX) and investor Maxit Capital (plus clients) taking a combined 14.4% stake in the business.

IENERGIZER +54%

Shares in call centre operator IEnergizer (IBPO:AIM) have had a rollercoaster two years: increasing five-fold in 2016 after falling 81% in 2015.

IEnergizer was the first India-based business process outsourcer to join London’s junior AIM market in 2010, raising $57m, and has enjoyed improving fortunes since the return in February of founder Anil Aggarwal to its chief executive role.

Business prospects look very good at iEnergizer: it delivered $10.2m of pre-tax profit in the first six months of 2016, up 10%, versus a market cap of $196m though we believe the company still has a bit to prove if it wants to attract new investors on to the shareholder register.

KEYWORDS STUDIOS +146%

We highlighted the investment attractions of video game designer and testing services provider Keywords Studios (KEYW:AIM) several times following its IPO (initial public offering) three years ago, including an extensive feature on the business and a recommendation to buy at 106p. The shares now trade nearly five times higher.

While we can claim credit for highlighting the stock before its significant rally, we do admit we’ve taken our eye off the ball in terms of coverage in 2016 – a year when the shares have shot up a further 146% to 502.5p.

We did meet chief executive Andrew Day a few times in the past 12 months, but didn’t feel compelled to write a new story.

Judging the sustainability of growth at highly acquisitive companies is difficult and particularly so in Keywords’ markets where key individuals can be important to business performance.

If key managers leave businesses acquired by Keywords, it could result in a drop-off in results, in our view. Keywords’ results have been impressive, however, delivering strong growth in underlying revenue and adjusted profit.

Its latest trading update (7 Nov) said full year pre-tax profit would be significantly ahead of expectations. To put that into context, the €14m pre-tax profit guidance from Keywords was 12% above consensus forecasts from analysts at the time.

Numis has a 555p price target for the shares over the next 12 months, implying the easy money has already been made from the stock. We do like the business; sadly the valuation is looking a bit high, trading on 26.5 times forecast earnings per share for 2017.

The big surge in earnings in 2016 has come from a business it acquired in April called Synthesis. Numis believes Synthesis’ results next year will be ‘well below 2016’, adding that it will have very tough comparative figures to beat as a result of large projects undertaken in 2016.

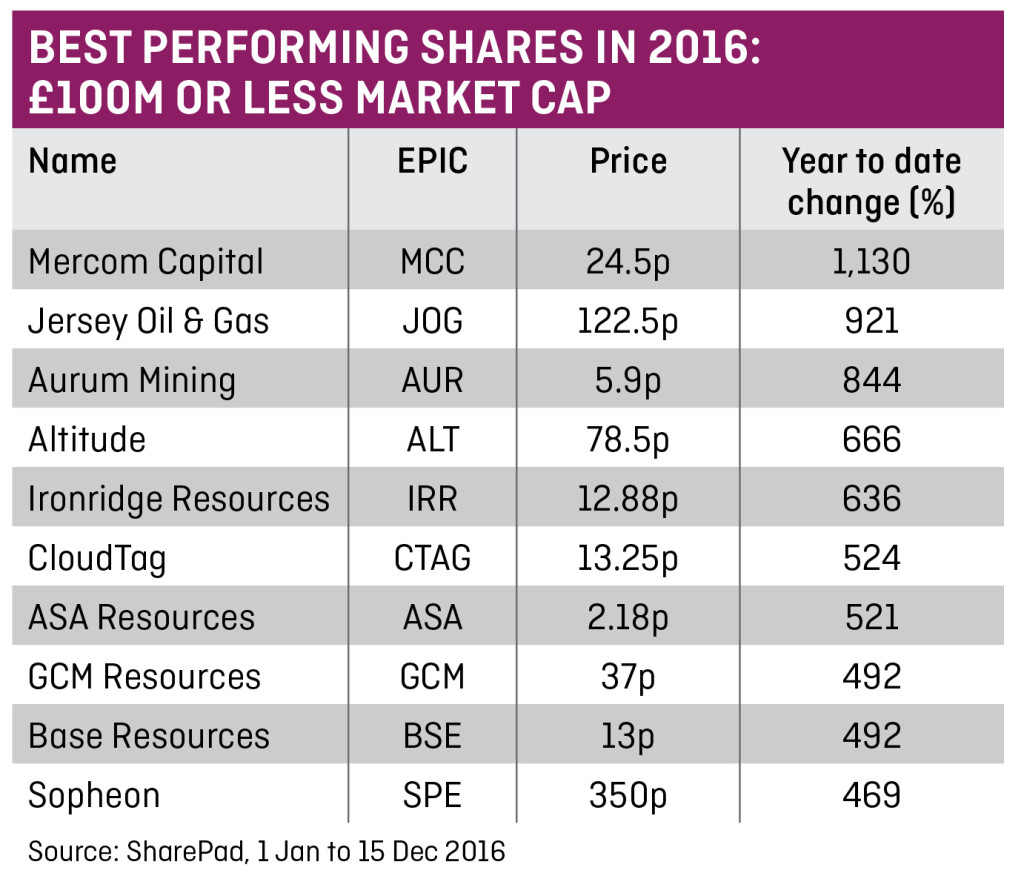

MARKET CAP £100m and below

JERSEY OIL & GAS +921%

The main driver behind the impressive share price performance of Jersey Oil & Gas (JOG:AIM) in 2016 is the farm-out deal agreed with Norwegian energy giant Statoil (STLO:STO). This deal, concluded in August, provides an endorsement of its flagship Verbier prospect in the North Sea and the impetus necessary to drill in the near-term.

Statoil has taken over operatorship of the well, Jersey retaining an 18% working interest, and has formally communicated an intention to drill in 2017 to the Oil & Gas Authority.

Jersey’s share of costs is covered after a £1.6m placing (30 Nov). We reckon there could be further upside to come as drilling approaches and the company begins to execute on a strategy of acquiring producing assets to make use of its £24m of tax losses.

ALTITUDE +666%

Marketing outfit Altitude (ALT:AIM) looked like it was going to the wall this time last year but a dramatic turnaround saved the business and returned it to profitability.

Speaking to chairman Peter Hallett earlier this year, we learned some of the gains may also be related to two new contract agreements Altitude signed with distributors of its products.

Altitude provides a software-as-a-service offering for small to medium-sized businesses in e-commerce. It also runs a big promotional products exhibition and runs websites for companies in the promotional products industry.

On a trailing 12 month basis, Altitude returned to profitability in June this year, having delivered almost £1m of operating profit across the second half of its 2015 financial year and the first half of 2016.

IRONRIDGE +636%

AIM-quoted IronRidge (IRR:AIM) went from being one of the worst performing IPOs of 2015 to one of the best performing small cap stocks in 2016. Although the shares started to rise in line with the sector earlier this year, the biggest acceleration came in July upon a strategy change.

Out went iron ore, in came gold. The market also liked an update on bauxite exploration, but the biggest cheer followed the acquisition of lithium projects.

This scatter gun approach is a sad reminder of how junior miners behaved in the last commodities bull-run, jumping on to whichever commodity was hot at the time. Ultimately success will come down to asset quality.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.