Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTop 10 for 2017

Every December we publish a list of stocks carefully chosen by Shares’ team of journalists. We consider these to be our best ideas for stocks to buy and hold throughout the coming year.

This year we’ve picked 10 companies that have the right qualities to shine in 2017.

You will find a mixture of top quality businesses, recovery stories and companies with favourable market conditions.

We will update on these stocks throughout the year in our Great Ideas section of the digital magazine and on our website.

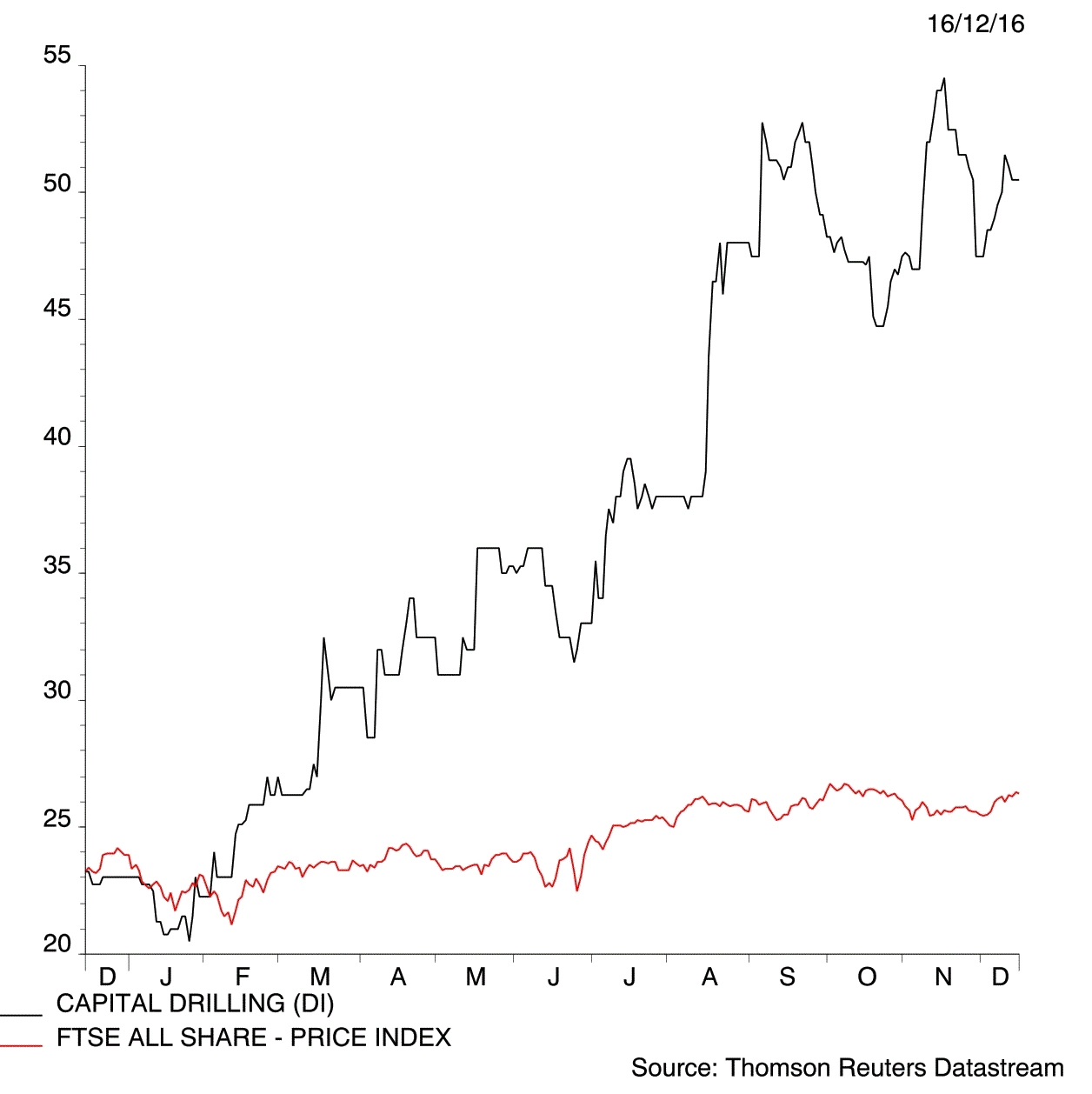

Capital Drilling (CAPD)

Share price: 49.9p

Market cap: £67.3m

EPS Dec 2017: 0.8c (0.6p)

PE Dec 2017: 83.2

Dividend Dec 2017: 4.4c (3.5p)

Dividend yield: 7%

Source: Shares, FinnCap

The increase in most commodity prices this year is driving renewed confidence in exploration spending by miners. That bodes well for a recovery in earnings at mining service group Capital Drilling (CAPD).

The business should benefit from a structural shift in the mining industry whereby companies are beginning to conclude asset disposal programmes and focus once more on increasing output and/or restarting growth projects.

Capital Drilling undertakes drilling work on both exploration prospects and operational mines. We believe its share price re-rating has only just begun in earnest.

Spare capacity

It should enjoy the benefits of operational gearing where any increase in revenue should essentially fall straight to the profit line. Only 43% of its fleet was being used, as of late October 2016. Therefore it has plenty of spare capacity to use existing drill rigs should it win additional contracts.

The pace of new work seems to be picking up. It has reported numerous contract awards over the past six months.

There are certainly positive signs in the market. For example, gold miner Acacia Mining (ACA) last month announced it would increase the amount of drilling in 2017 year-on-year by approximately 40% to 190,000 metres across its sites, and has budgeted $25m for the work.

Acacia is an existing client and has already asked Capital Drilling to undertake more exploration drilling in Kenya, as per a new contract award in September. Other clients include Centamin (CEY), which remains very active in Egypt and parts of West Africa.

We see positive signs elsewhere in the industry, all pointing towards greater volumes of drilling work. For example, FTSE 100 diversified miner BHP Billiton (BLT) said it would spend $800m on exploration in its 2017 financial year.

At the lower end of the market spectrum, we note a recent report from accountancy firm BDO that found Australia-based junior miners increased their exploration spend quarter-on-quarter in the three months to September, only the second time in more than two years.

Earnings recovery

Broker FinnCap forecasts Capital Drilling will make $4m pre-tax profit in 2017. In October it set a 70p price target for the next 12 months, implying 40% share price upside.

The dividend policy is paying 25% to 50% of free cash flow. Forecast payment of 4.4c (3.5p) implies 7% prospective yield for 2017. (DC)

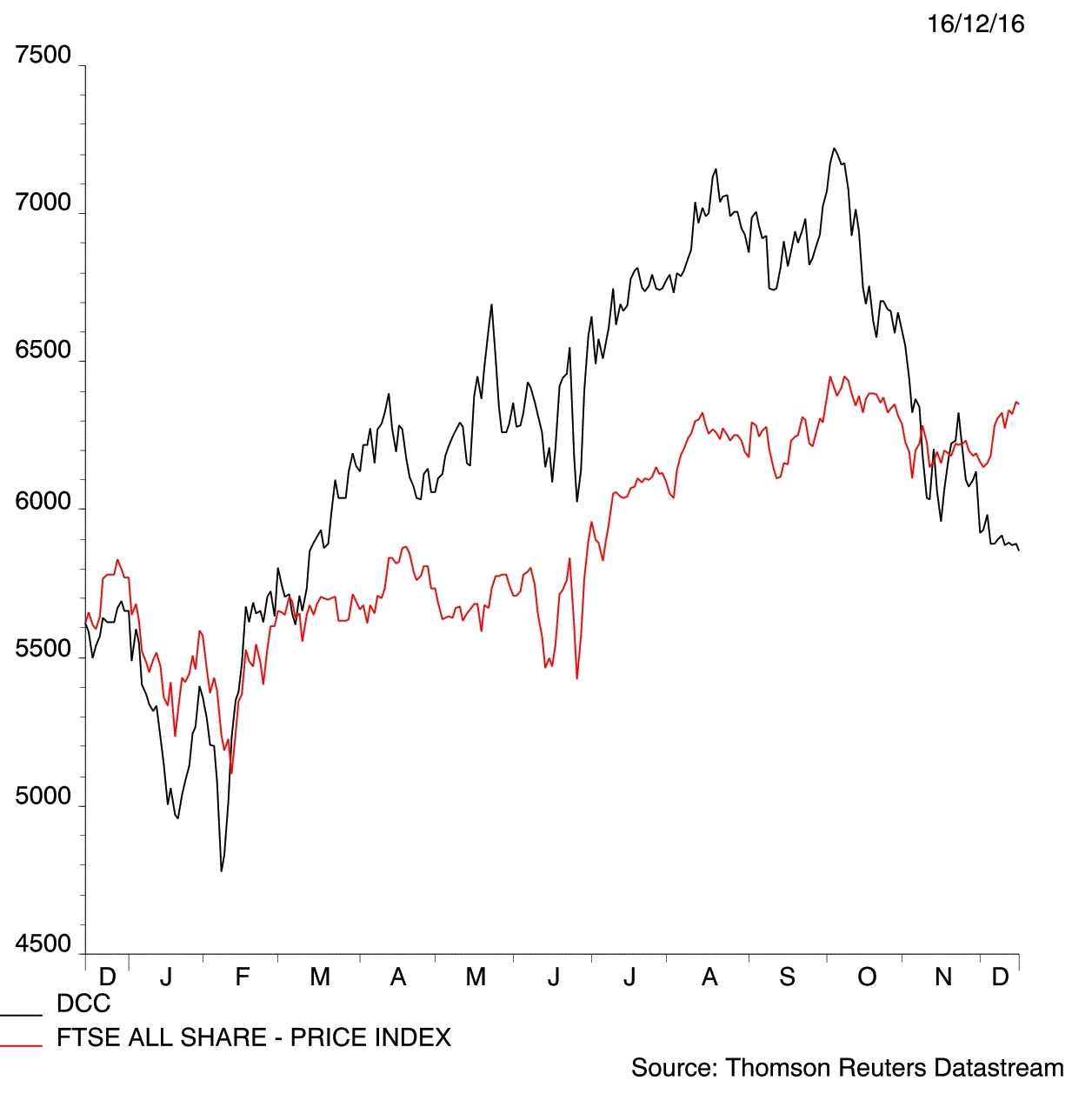

DCC (DCC)

Share price: £58.50

Market cap: £5.17bn

EPS Dec 2017: 298.8p

PE Dec 2017: 19.6

Dividend Dec 2017: 113p

Dividend yield: 1.9%

Source: Shares, Jefferies

The energy, healthcare and technology products distributor ticks all the right boxes for a superior investment. It has a disciplined approach and only undertakes acquisitions or projects when it sees scope for a decent return on investment.

Recent share price weakness looks unwarranted and provides a good opportunity to buy a brilliant company at its cheapest level for nearly a year.

DCC has a superior track record for dividend growth. We calculate that £5,000 invested 10 years ago with all dividends reinvested would now be worth a fantastic £23,308.

Two thirds of DCC’s profit comes from the energy sector. It distributes liquid petroleum gas and oil to customers across Europe. DCC also operates 825 retail petrol stations; some unmanned.

Furthermore, it markets and sells branded fuel cards to industrial and commercial fleets, giving them discounted fuel. This is a UK-only proposition at present, yet analysts expect DCC to roll out the offering across Europe given it is highly profitable and DCC can leverage its investment in retail networks.

Healthy future

The healthcare business has the highest organic growth potential, according to broker Canaccord Genuity. This division sells a range of own-branded and third party medical and pharmaceutical products to the likes of pharmacies, hospitals and doctors’ surgeries. It also sells medical devices and consumables like gloves.

DCC provides contract manufacturing services to the health and beauty industry across Europe, mainly focused on areas like vitamins and skin care products. It is well placed to benefit from the trend among health and beauty brand owners to outsource non-marketing and sales operations.

The technology division sells products from over 350 suppliers to specialist retailers, grocers and resellers. This business is more cyclical than the rest of the group so earnings do occasionally dip.

There is also a waste management business in DCC although it only contributes a small amount to group profit.

Strong balance sheet

Analysts believe the best acquisition opportunities for DCC will be in the energy segment as large oil firms continue to sell non-producing assets to help reduce their high debt levels.

DCC has plenty of firepower to continue making acquisitions. Net debt at its half year stage was only £112.2m. In comparison, it generated £291.1m free cash flow in the financial year to 31 March 2016. (DC)

Devro (DVO)

Share price: 165.5p

Market cap: £282m

EPS Dec 2017: 15.3p

PE Dec 2017: 10.8

Dividend Dec 2017: 9p

Dividend yield: 5.4%

Source: Shares, Investec Securities

Sausage skins maker Devro (DVO) could serve up some sizzle in 2017. We believe the shares have been oversold following a recent setback and view the company as having tasty longer term growth prospects.

Devro supplies collagen casings for sausages, salamis and hams. It has a demonstrable ability to differentiate products in its global market place.

It is geared into burgeoning global demand for collagen casings linked to higher protein consumption in emerging markets.

Yet it also faces some challenging market conditions caused by geopolitical factors, changing eating habits and retailers putting the squeeze on meat suppliers.

Two warnings

In August, Devro cautioned that a transitional period would be needed to extract the benefits from £110m worth of new plant investment in the US and China to position it for growth in the future.

On 10 November, it warned 2017 profit would disappoint and debt, taken on to invest for growth in China and the US, was close to breaching commitments given to lenders.

Seeking to mitigate weaker volume trends in China, Russia and Latin America, the food producer warned it would accelerate restructuring plans and make investments in next generation products to improve its competitive position.

This investment will partially offset 2017 volumes which will now be 10% lower than previous expectations. The result is under-utilisation of manufacturing capacity and crimping margins.

Nevertheless, investors with risk-appetite might view this as a great time to pounce. Devro’s disappointments are largely discounted on a grudging 2017 prospective multiple of 10.8 times and a 5.3% dividend yield based on Investec Securities’ estimates.

Resilient performance

Analyst Nicola Mallard remains a buyer and her 270p price target implies 63% upside.

She forecasts £31.5m pre-tax profit (2015: £31.3m) for the 2016 financial year. This rises to £33m in 2017.

Directors including chief executive Peter Page and chairman Gerard Hoetmer wasted no time buying shares with their own money following the recent sell-off.

Devro might even draw takeover interest should the share price weakness persist. Spanish rival Viscofan (VIS:MC) is one name potentially in the frame. (JC)

Hotel Chocolat (HOTC:AIM)

Share price: 281.5p

Market cap: £321.7m

EPS June 2017: 7.4p

PE June 2017: 38

Dividend June 2017: 1.5p

Dividend yield: 0.5%

Source: Shares, Liberum Capital

Don’t be put off by Hotel Chocolat’s (HOTC:AIM) low dividend yield and high price to earnings ratio. We believe it is a very interesting investment proposition with the potential for rapid earnings growth.

The premium British chocolatier and omni-channel retailer is taking share from sleepy incumbents such as Thorntons. It has enjoyed earnings upgrades in 2016 and we believe that trend will continue in 2017.

Guided by co-founder and chief executive Angus Thirlwell, Hotel Chocolat offers customers accessible luxury at affordable prices through its own stores, cafes and boutiques.

Earn again and again

It boasts a strong digital business that includes the innovation-driving, recurring revenue-delivering ‘Tasting Club’. This is a subscription service where circa 70,000 members pay £22.95 a month to be the first to try the company’s newest chocolate products.

One of few chocolatiers to actually grow cocoa, its competitive advantages feature a vertically-integrated supply chain and strong intellectual property in the form of internally-created recipes.

The £321.7m cap offers exposure to double digit earnings growth through the roll-out of stores, which act as showrooms that prompt customers to subsequently make future orders online.

The business is also strongly cash generative, which means it can self-fund expansion and progressive dividends are on their way.

INTERNATIONAL OPPORTUNITY

> £70bn market

------------------------------

Hotel Chocolat has >0.02% market share

Source: Hotel Chocolat annual report

Large opportunity

Spearheading the rise of craft-style and artisanal chocolate making, Hotel Chocolat has a very modest share of the £7.6bn UK chocolate market and big potential in a £20bn UK gifting market. There is even more to go for overseas.

The brand resonates with consumers as original, authentic and ethical. The company’s ‘more cocoa, less sugar’ mantra means Hotel Chocolat is geared into the wellness consumer trend and appeals to UK and overseas shoppers alike. We expect the weak pound will stimulate sales to foreign visitors through its travel stores.

House broker Liberum Capital forecasts adjusted £10.2m pre-tax profit for the year to June 2017 and a maiden 1.5p dividend. These metrics are estimated to rise to £11.1m and 1.6p respectively in 2018. (JC)

Ideagen (IDEA:AIM)

Share price: 64.25p

Market cap: £117m

EPS Apr 2017: 3.2

PE Apr 2017: 20

Dividend Apr 2017: 0.2p

Dividend yield: 0.3%

Source: Shares, FinnCap

There’s a net of rules, regulations and red tape tightening over many industries. Little UK software supplier Ideagen (IDEA:AIM) has a wide range of off-the-shelf specialised software tools smack bang in this, albeit unglamorous, sweet spot.

The Midlands-based company concentrates on what it calls the governance, risk and compliance (GRC) space, providing information management solutions to highly regulated industries.

Target markets include healthcare, complex manufacturing, banking/finance, defence and energy.

Ideagen supplies an integrated system that combines information from multiple operational sources on top of the typical internal audit and compliance functions.

This provides clients with a detailed overview of corporate risk, controls and consequence mitigation analysis.

That’s an increasingly compelling sale once an organisation begins to grasp the significant financial and reputational damage potential of not having adequate systems in place.

Loyal fans

We’ve been fans of the company since it gravitated to AIM from the old Plus Markets in 2012, first flagging the investment opportunity at 16p in August that year.

The company hasn’t put a foot wrong ever since; adding carefully vetted bolt-on acquisitions to its underlying progress. Three acquisitions have been made since summer 2016 alone, being Covalent, Logen and IPI Solutions.

Full year results to 30 April 2016 revealed a 52% revenue jump to £21.9 million including respectable 10% organic growth. That led to a 57% leap in adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) to £6.3 million and improved operating cash conversion metrics.

Shareholders should feel rightly chuffed about a 96% client renewals hit rate and 100 new customers won during that year.

Ideagen also won its biggest single contract ever, worth £4.9 million. We believe the scale of new business is also improving.

Healthy and wealthy

A trading update in November implies the business is still in excellent health. We’ll find out more when half year results are published in January.

FinnCap forecasts pre-tax profit rising by 21% to £6.9m for the full year to April 2017 – and then advancing to £8.4m a year later.

It is also worth noting that Ideagen could potentially benefit from Brexit as that will increase red tape. Companies will need to comply with existing EU and international standards as well as the potential for the implementation of UK standards. (SF)

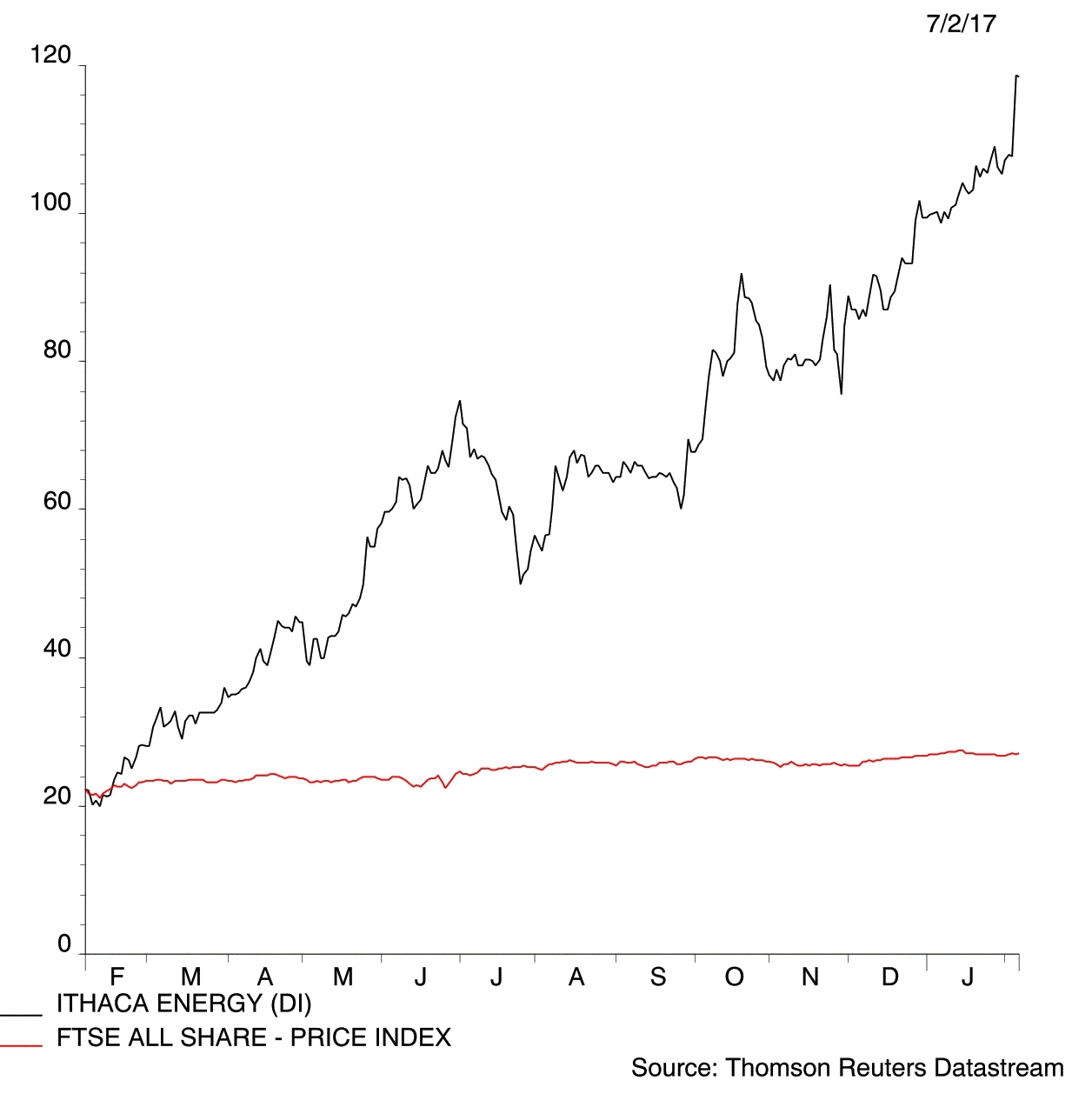

Ithaca Energy (IAE:AIM)

Share Price: 86p

Market cap: £355m

EPS Dec 2017: 12p

PE Dec 2017: 7.2

Dividend Dec 2017: n/a

Dividend yield: n/a

Source: Shares, Macquarie

There is clear line of sight to considerable share price upside at North Sea oil producer Ithaca Energy (IAE:AIM) as its flagship Stella field comes on stream in January 2017.

A more than doubling of production should boost earnings and give Ithaca the means by which to rapidly pay down debt.

Its shares have advanced more than 200% in 2016 thanks to leveraged exposure to oil price recovery and progress towards first oil from Stella. This is worth putting into context; the stock is still some way below the 200p-plus levels it hit back in 2012.

We think there will be further strengthening in the crude market in 2017 as the oil price begins to reflect a tighter supply situation.

Highly leveraged to the oil price

Like other indebted names in the sector Ithaca is likely to rise on a higher oil price, but its balance sheet looks a much safer prospect than peers such as EnQuest (ENQ) and Premier Oil (PMO).

Getting Stella on stream has been a complicated business, with the latest setback pushing start up on the field from the end of November 2016 to January 2017. It originally had a start date in the first half of 2014.

With operations finally up and running, the company’s output should hit a net 20,000 to 25,000 barrels of oil equivalent per day (boepd) from the current 9,500 boepd.

Debt reduction

Upfront capital expenditure has been sorted and operating costs have successfully scaled back to less than $20 per barrel of oil equivalent. The company should therefore generate plenty of cash flow to pay back its net debt.

Canaccord Genuity reckons borrowings will fall 30% to around $400m by the end of 2017.

This should create the headroom to pursue and acquire additional projects which can share Stella’s infrastructure, made up of a floating production facility and link to a nearby oil pipeline. In turn this can further reduce costs and boost cash flow.

The company already has at least two likely additional tie-back projects in the so-called ‘Greater Stella Area’, called Harrier and Vorlich. Tie-backs refer to the connection of additional fields to a floating vessel or platform. (TS)

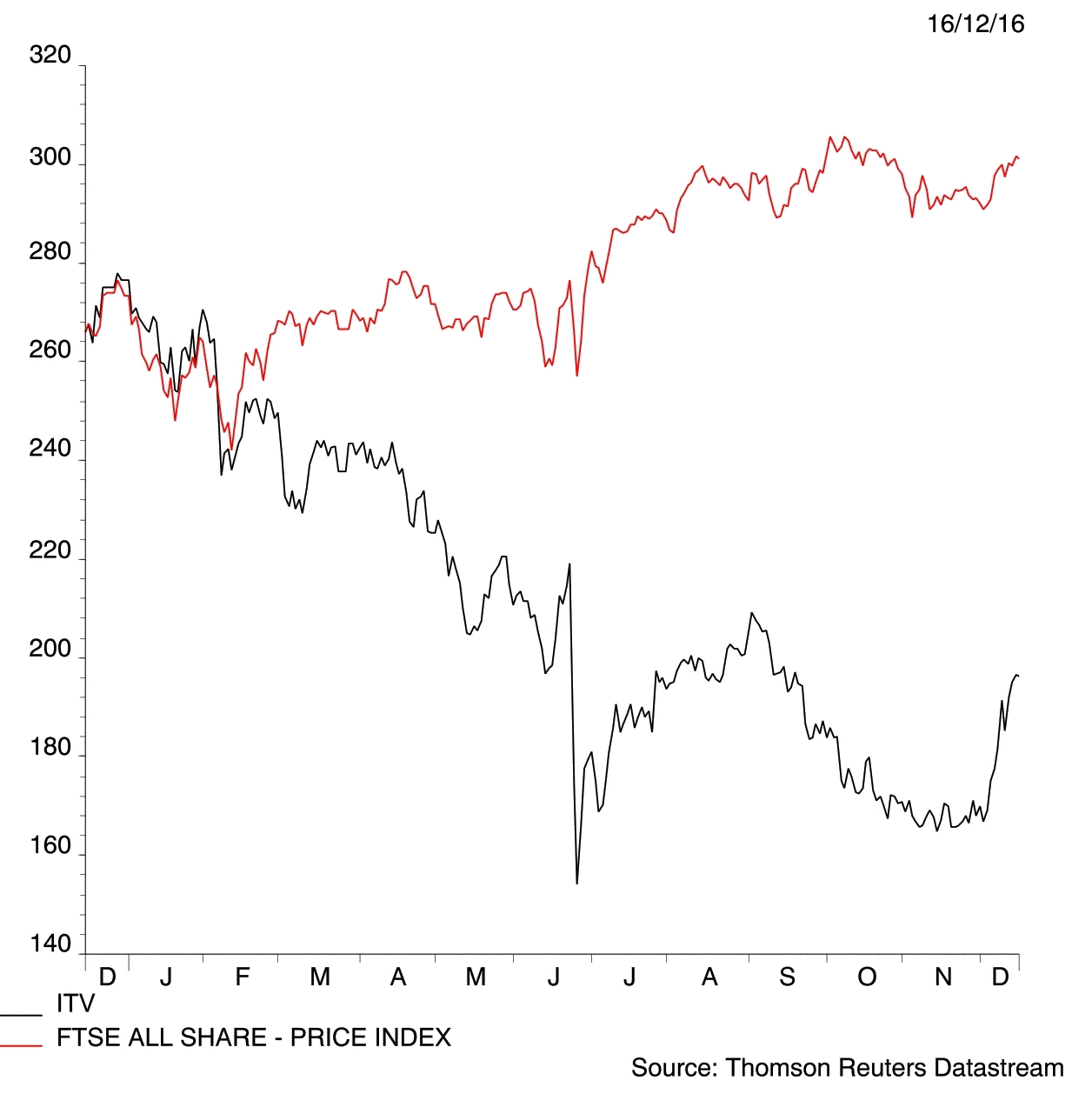

ITV (ITV)

Share Price: 194.6p

Market cap: £7.8bn

EPS Dec 2017: 16.1p

PE Dec 2017: 12.1

Dividend Dec 2017: 9p

Dividend yield: 4.6% (excludes special dividend)

Source: Shares, Thomson Reuters

Notwithstanding a return of share price strength since early December, a UK advertising slowdown looks more than priced in at free-to-air broadcaster ITV (ITV).

We think this well-run and one-of-a-kind business could do rather better than the market thinks in 2017. We believe analysts will upgrade earnings forecasts which could help to drive up the share price further.

Assuming no year-on-year change in the ordinary or special dividend from a highly cash generative business, ITV also offers a prospective yield of nearly 9%.

The yield would still be attractive at circa 4.6% even if it didn’t pay a special dividend.

Consensus bearish

Analysts expect ITV to experience a 4% decline in TV advertising revenue in 2017. Admittedly the coming 12 months could be tough if the UK consumer scales back spending amid a dark cloud over the economy and rising inflation.

We still see reasons to back ITV’s management claim alongside third quarter results that it can outperform the wider market.

Data quoted by Liberum shows ITV1’s audience share up nearly 30% year-to-date (as of 27 November) against a flat Channel 4 and Five down 3%. This should translate into a greater slice of the TV advertising pie.

More generally TV remains a very effective means of advertisers getting their message across to consumers. It is more transparent than online advertising where there are growing fears that advertisers are essentially being defrauded.

To reduce its reliance on ads, ITV has made a number of acquisitions to bolster its production business and build up its content portfolio.

Takeover talk

The share price has responded in the wake of 21st Century Fox’s (FOX:NYSE) £18.5bn bid for Sky (SKY). Investors are betting ITV could be next on the block.

Like Sky, ITV is a unique asset on the UK market with a depressed share price. US-based Liberty Global (LBTYA:NDQ) has a 9.9% stake and is a logical suitor, particularly given the weakness of the pound.

Liberty chairman John Malone has been quoted as being interested in gaining exposure to the UK advertising market and is encouraged rather than put off by the Brexit vote. (TS)

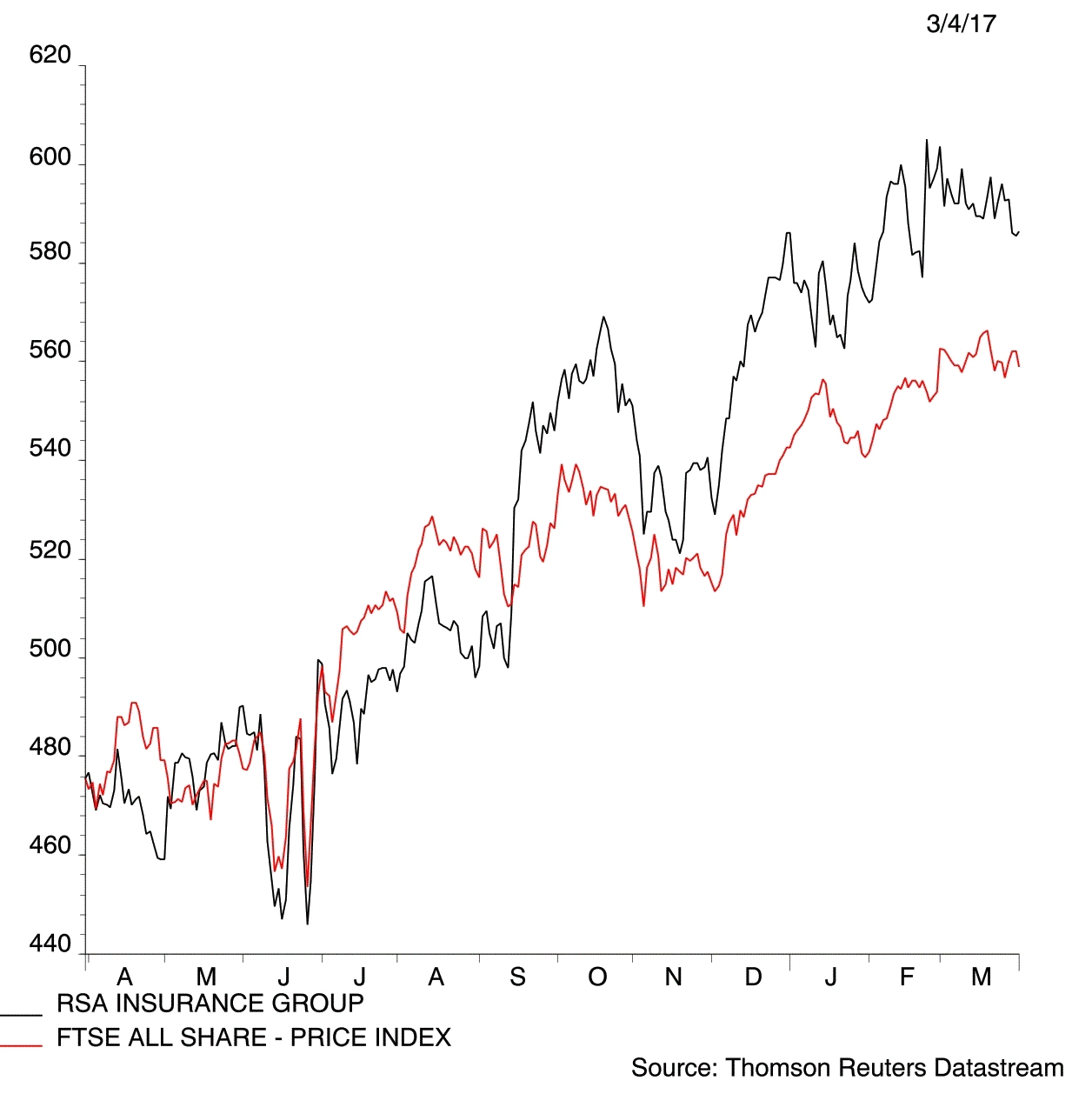

RSA Insurance (RSA)

Share price: 565p

Market cap: £5.8bn

EPS Dec 2017: 46.3p

PE Dec 2017: 12.2

Dividend Dec 2017: 20.8p

Dividend yield 2017: 3.7%

Source: Shares, Panmure Gordon

RSA Insurance (RSA) is on its way back to becoming a world class insurance business. Founded in 1706, RSA’s history is an indicator of the enduring importance of the insurance industry as well as its ability to bounce back from the occasional problem.

Chief executive Stephen Hester, previously fire fighter-in-chief at Royal Bank of Scotland (RBS), joined the business after poor performance and financial irregularities in its Irish unit led to a board room purge in late 2013.

Now two years in to the turnaround plan, RSA is delivering tangible progress on its road map to becoming among ‘the highest performing and best valued companies in our industry’, according to Hester.

Property and casualty insurance companies like RSA usually have two key drivers of their stock market performance: insurance underwriting performance and investment returns.

Underwriting improvement

Writing profitable insurance policies requires pricing discipline in tough markets as well as a laser-like focus on costs.

Hester is delivering both factors. RSA is passing up the opportunity to write more insurance policies so it can focus on parts of the market where pricing enables the business to deliver acceptable returns.

An insurer’s combined ratio (COR) is the ultimate measure of underwriting quality.

A combined ratio is a type of cost-to-income ratio. RSA’s underwriting costs in the first half of 2016 were 94.3% of the insurance premiums it received. That’s a bit like saying it had an operating profit margin of 5.7%.

Investment portfolio

Insurers receive premiums upfront and pay claims later, meaning they generate a large amount of capital to invest. RSA invests this capital mainly in investment grade bonds in the regions where it operates: the UK, Scandinavia, Canada and Ireland.

Investment returns are an important part of performance at insurance companies. RSA’s portfolio totalling £14.6bn delivered income of £187m in the six months to 30 June 2016, more than its underwriting profit of £119m.

On top of that, RSA enjoyed capital gains as interest rates fell, which pushes up the value of bond prices. It is likely the value of RSA’s bond portfolio will have declined in recent months as interest rates in many countries started to rise.

While this is a short-term negative, RSA’s future is now much more in its own hands as a better focused business delivering decent underwriting performance, in our view. (WC)

Serco (SRP)

Share price: 141p

Market cap: £1.6bn

EPS Dec 2017: 2.7p

PE Dec 2017: 52.2

Dividend Dec 2017: n/a

Dividend yield: n/a

Source: Shares, Liberum

Outsourcer Serco (SRP) may represent a defensive 2017 opportunity as its business reorganisation takes shape over the next year.

It was the best performer in our ‘Big picks for 2016’ portfolio, enjoying a solid year of profitability. We’ve decided to include it in our new ‘picks of the year’ portfolio in the belief the market will focus in 2017 on Serco’s growth prospects rather than its past problems.

Wheels in motion

Serco’s investment case centres around a business plan laid out by chief executive Rupert Soames in late 2014 which outlined a case for long-term top-line growth of 5% to 7% with operating margins between 5% and 6%.

Revenue looks set to bottom out in 2017 at a little under £3bn. Patient investors could be rewarded if the business can begin to sustainably earn and grow operating profit from the base of between £100m to £150m implied by its margin ambitions.

Evidence Serco is beginning to win favour with customers once more include a 10-year, £600m framework agreement signed with Barts Health NHS Trust, England’s largest, on 1 December.

Analysts at Liberum do not expect Serco to be able to deliver its target margin range until around 2020 but say the NHS contract win indicates it may now be out of the Government ‘sin bin’ for major new contracts.

‘Management have a clear esprit de corps,’ writes analyst Joe Brent in a 2 December commentary. ‘They tell us the leadership engagement scores have increased from 38% in 2014 to 72% in 2016. They have adopted a style of “disciplined entrepreneurialism”.

He adds: ‘The IT systems are much improved and management have much better grasp of service line costs and overheads, which helps to price contracts correctly.’

Stay alert

Key risks centre on the potential for a repeat of contract flare-ups which previously scuppered Serco’s profitability and forced a rights issue in early 2015.

Outsourcing businesses in Serco’s market earn thin margins and cost pressures or unexpected revenue declines can lead to large share price swings, as has been the case at rivals Interserve (IRV) and Capita (CPI).

Brent also flags a potential reduction in funding for Obamacare in the US after the election of Donald Trump. Serco undertakes some administration work for the healthcare scheme.

‘We expect Trump is positive for defence spending and negative for Obamacare, a top five contract by revenue, even though it is likely Obamacare will continue to exist in some form,’ adds Brent. (WC)

Tracsis (TRCS:AIM)

Share price: 520p

Market cap: £142.2m

EPS Jul 2017: 24p

PE Jul 2017: 21.7

Dividend Jul 2017: 1.4p

Dividend yield: 0.3%

Source: Shares, Reuters Eikon

We are hopeful for a meaningful US breakthrough on the remote condition monitoring (RCM) rail track side for Tracsis (TRCS:AIM) in 2017.

With its first major order secured in August 2016 for RCM software and hardware kit we wouldn’t be surprised to see other contracts fall into place over the coming 12 months.

The company’s clever RCM kit use sensors, black boxes and wireless connectivity to assess thousands of points, tracks, cabling, level- crossings and more from a central control room.

Stresses can be spotted early and maintenance people directed to exactly the right problem in a fraction of the time, saving money, cutting workloads and boosting safety standards.

At a rough 140,000 miles of track, the US railroad network is about seven-times the size of the UK’s so the potential is enormous.

Intelligence recognised

We also anticipate plenty of progress elsewhere as the Leeds-based company bulks up its intelligent transport infrastructure technology, particularly now that Tracsis is recognised as a traffic data intelligence and analysis play.

This is a high quality business. It looks like 2016 will be the first in five years when the share price hasn’t shown annual gains – putting up returns of 188%, 24%, 106% and 26.5% between 2012 and 2015. We don’t see that as reason to worry.

Deal maker

Tracsis has a good track record when it comes to making acquisitions. They always seem to enhance profit and cash generation. Deals tend to be self-funded with minimal or zero dilution to shareholders.

The latest acquisitions have beefed up the railside (Ontrac) and the traffic data division (SEP). Tracsis has the ambition and financial muscle for more deals.

In the year to 31 July 2016 it generated £7m of cash, bulking its bank balance to £11.4m. It has no debt. Analysts forecast mid-single digit revenue growth in the current financial year to £34.7m, implying £8m of pre- tax profit and a 17% hike in the dividend to 1.4p per share.

A year seldom passes without analysts upgrading their earnings estimates, often multiple times. The current price to earnings ratio is 21.7. Tracsis has a superior track record of delivering top returns which justifies a premium rating. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.