Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShares’ 2016 Picks in Review

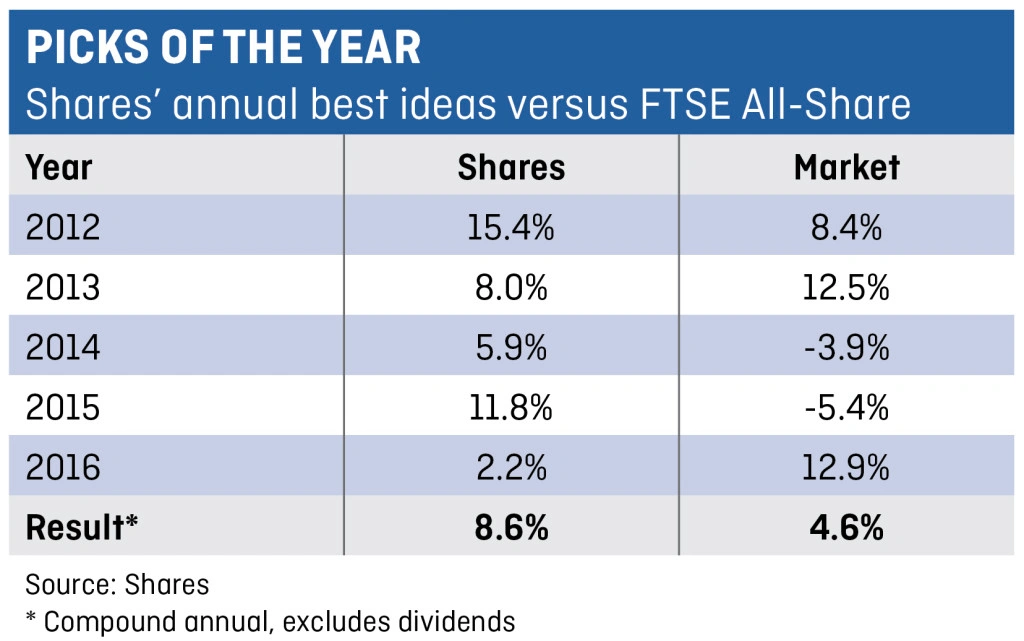

Our ‘Big Picks for 2016’ portfolio gained an average of 2.2% versus a return on the FTSE All-Share of 12.9%. It’s a disappointing performance compared to previous years, but at least we didn’t lose money.

After a decent start to the year, in which our stocks led the market in very tough conditions, it’s tempting to blame Brexit for the reversal which started in June. But that would not be entirely fair.

Most of our bigger losers this year were hit by business problems which hurt their profitability and stock market performance.

Sometimes economic factors contribute to poor returns but in 2016 the main drag among our picks was simply that the businesses we selected were not of high enough quality.

We’ve learned our lesson: Shares’ 2017 selections undoubtedly contain more star quality than last year’s. They include DCC (DCC), Tracsis (TRCS), Devro (DVO), ITV (ITV) and RSA Insurance (RSA).

While a 2.2% result is disappointing against a bigger gain from the wider market, it’s the first time Shares’ tips of the year have trailed the benchmark since 2013. It’s also our fifth positive result in a row.

Here’s what went right and wrong for Shares’ 2016 picks and what we learned this year.

A few positives

Shares’ top gainer in 2016 was public sector outsourcer Serco (SRP), which gained 48.9%.

Serco started to mend its relationships with customers after a long-running slump which began when it was revealed to have overcharged the UK Government on electronic tagging contracts for prisoners.

Chief executive Rupert Soames says the business is nearing the end of a period which has seen contract wins dry up and revenue fall, an inflection point which has driven Serco’s share price higher this year.

Profitability also helped. Analysts expected Serco to deliver a £50m trading profit in 2016. Soames is now saying the business will earn ‘not less than’ £80m.

Guidance for 2017 has not changed, however, meaning the next 12 months are likely to see a continuation of revenue declines and a moderate fall in profitability before a hoped-for return to growth in 2018.

Commodities rally

Another winner was oil producer BP (BP.). It gained 40% as a wobble in commodity markets early in 2016 reversed and key crude oil benchmarks posted their first year-on-year gains for around two years in late 2016.

Picking BP was a particularly bold call in early 2016 when the sentiment towards oil stocks was especially poor and credit goes to our oil and gas sector specialist Tom Sieber for seeing through that short-term sentiment.

Other gainers which made it into double digits include Telecom Plus (TEP), BCA Marketplace (BCA) and Breedon (BREE:AIM).

Lessons learned

Leading the losers was micro cap digital marketing stock Eagle Eye Solutions (EYE:AIM), down 44.3% over the 12 months. It provides retailers and suppliers of fast moving consumer goods with the ability to generate digital coupons which can be tracked more easily when redeemed by customers.

Revenue was expected to hit £8m in the year to 30 June 2016 but the actual number, announced in a trading update in early June, came in at just £6.5m. While this represented growth of 34% from a year earlier, investors were unimpressed that key contracts had been delayed.

Even so, Eagle Eye has an impressive management team and board line-up and claims it is now close to break-even profitability, an outcome expected sometime in 2017. And it is still growing quickly.

Lender Shawbrook (SHAW) was another disappointment. Financial stocks struggled after the UK’s vote to leave the EU but Shawbrook’s problems were self-inflicted.

It revealed a £9m irregularity on loans in its asset finance division and investors justifiably marked down its share price. While £9m is not huge for a company the size of Shawbrook, the issue badly dented confidence in the business.

Convenience foods seller Greencore (GNC) was another disappointment, down 29%. The stock was doing nicely until it raised equity via a discounted rights issue to fund the $747.5m (£594.3m) acquisition of US-based Peacock Foods.

If we adjusted the performance of Greencore for the value of the rights attached to its shares, the overall return on Greencore would be minus 11% rather than minus 31%. That would have increased our overall result from 2.2% to 3.7% this year. (WC)

Disclosure: The author owns shares in BP.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.