Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGet to grips with pension deficits

Underfunded pension schemes have become a political football since BHS failed under the weight of its pension deficit.

Many companies listed in the UK – particularly large businesses founded many decades ago – also have large pension obligations to employees.

Understanding a few simple rules can help investors weigh up the risks around a company’s pension deficit and decide whether the risk is worth taking.

There’s no need to be an actuary to understand the basics of a corporate pension scheme. We use the example of telecoms giant BT (BT.), which has the UK’s largest defined benefit pension scheme, to run over some of the key points.

Rule One – Understand the assets

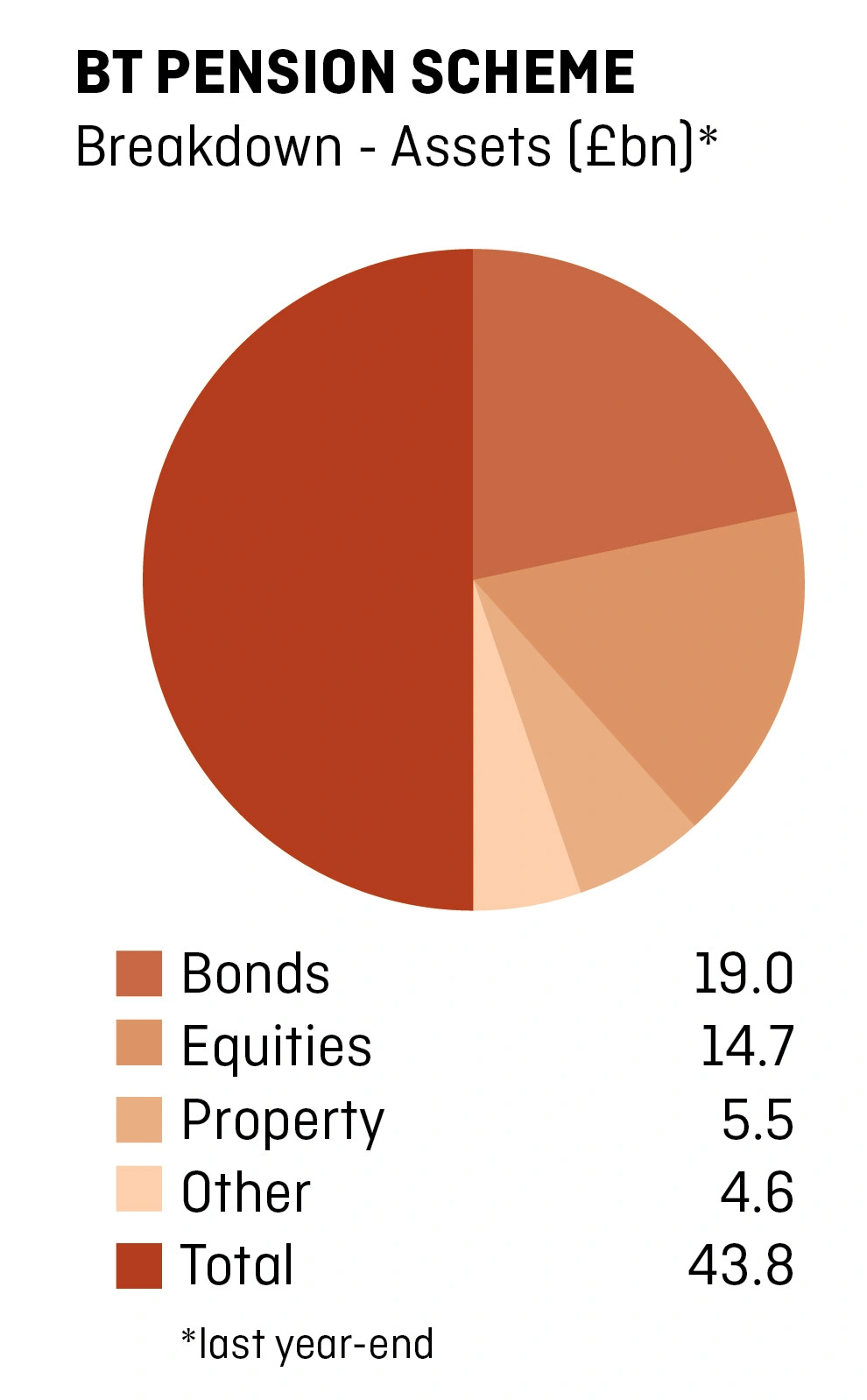

Pension scheme assets are straightforward. All of the assets which have been accumulated by BT’s pension scheme over the years equal £44bn, an amount bigger than the company’s entire market capitalisation of £36bn.

These assets are amounts BT has set aside in the past to cover its future obligations to pensioners. Included in these assets are £14.7bn of equities, £7.3bn of bonds, £11.7bn of property assets and £4.6bn of other assets including emerging market debt.

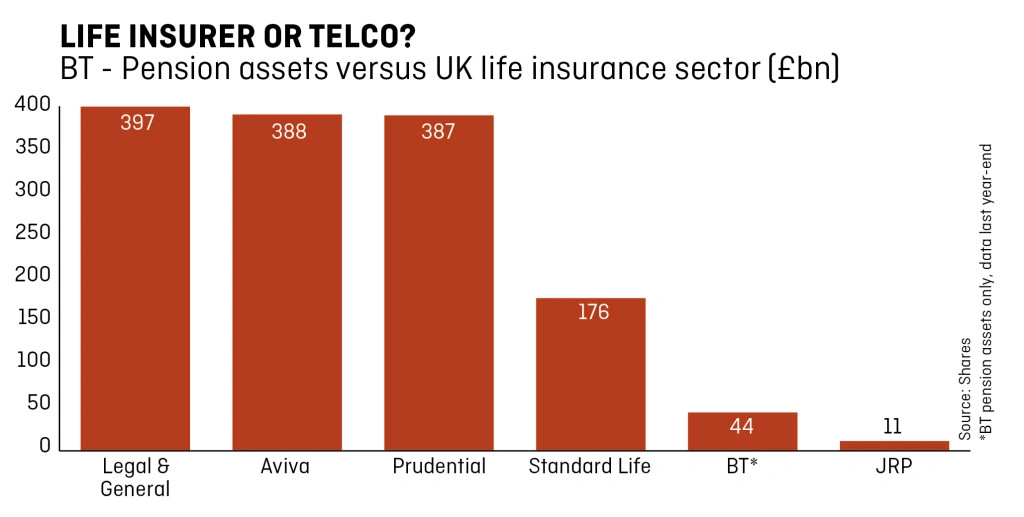

In total, BT’s pension fund assets are around one-tenth the size of Legal & General’s (LG.), one of the UK’s largest life insurance companies.

Unfortunately, it’s still not enough!

Rule Two – Understand the liabilities

Even with £44bn of assets, BT’s pension assets are £6.4bn lower than its reported liabilities. BT’s pension scheme liabilities are estimated by actuaries at £50.4bn.

Liabilities, importantly, are estimates. The best way to understand pension scheme liabilities is to consider them as an estimate of how much a company would need today to meet pension future payments assuming the company’s assets were invested in corporate bonds.

Within these estimates, which are common to all pension schemes, are:

• Estimated inflation

• Estimated life expectancy

• Estimated returns on corporate bonds

After compiling all of these estimates, as well as a few minor additional ones, BT’s pension liabilities are £50.4bn on an accounting basis.

Changes in the assumptions alter the estimate of the liability. An increase in expected inflation or life expectancy increases the liability. On the corporate bond assumption, falling corporate bond yields reduces the expected return on bonds and increases the size of the liability. This is why companies often refer to falling bond yields when they talk about why their pension liabilities and deficit have increased.

Rule Three – Understand the deficit

Pension assets minus liabilities equals the estimated account deficit. Tax reduces the deficit somewhat because corporate payments into a pension scheme attract a tax break. In BT’s case, the value of this tax break is about £1.1bn.

Eagle-eyed readers may have spotted there is one glaring difference between the accounting estimates used to calculate BT’s pension liability and the economic reality of how the scheme is run.

Pension liabilities, the amount BT must have to fund its pension obligations, are calculated as if the company’s pension scheme was invested in corporate bonds.

In reality, the assets in its scheme are invested around one-third in equities, 43% in a mix of bonds and the remainder in other assets.

Investment implications

This has a few important implications for investors in BT and other companies with large pension deficits.

For example, holding all other variables constant, a gain in BT’s equity portfolio of around 44% would wipe out its entire £6bn-plus pension deficit. That’s not an implausible scenario – it could happen in one year if the stock market had a particularly good run.

Equally, if global equities declined by a similar amount, BT’s deficit would increase by a little over £6bn, doubling the size of the deficit.

This is an important factor for all companies with pension schemes which have some or all of their assets invested in equities.

Movements in the general stock market – other company’s share prices – have at least as big an impact on companies like BT as their own performance in providing telecoms services, for example.

If a large number of companies listed on the stock market, as they do in the UK, have big pension deficits, a falling stock market may become self-fulfilling to a certain extent. The stock market falls, pension deficits widen, share prices of companies with pension deficits fall – which causes the stock market to fall further.

The opposite is also true: if share prices rally even modestly over the next few years, pension ‘black holes’ will be out of the newspapers for good. Companies and the government might even start to wonder if defined benefit plans are a good idea again.

While this is a hypothetical argument – by changing only

one variable in a complex set of interrelated factors – it is worth thinking about when picking stocks.

As an investor, ensuring your portfolio is well diversified not just by sector but also by limited overall exposure to companies with large pension deficits or other balance sheet risks could help you enjoy more stable stock market returns.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.