Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAll rise for Reckitt

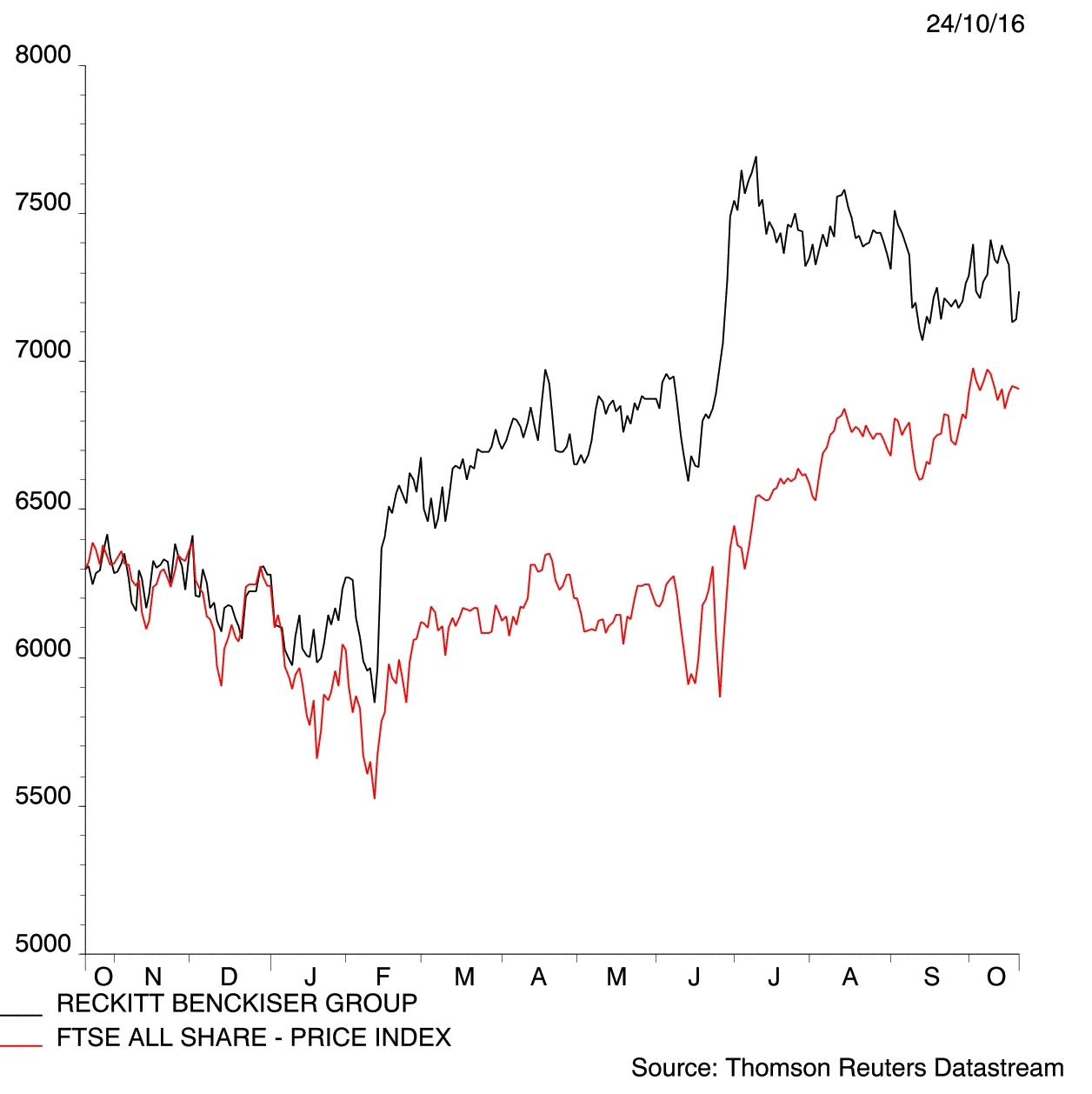

A pull-back at consumer products colossus Reckitt Benckiser (RB.) following a disappointing third quarter update (19 Oct) presents a buying opportunity.

With slower end markets and a South Korean humidifier sanitiser issue hogging headlines, it is easy to overlook the fact that earnings per share remain very much in an upwards trajectory, highlighting the resilience of the globally-diversified consumer brands business.

Damaging downgrades

Reckitt Benckiser downgraded 2016 like-for-like revenue guidance from 4-5% to 4% following its Q3 like-for-like sales miss. The FTSE 100 giant’s reputation has taken a hit in South Korea, where more than 100 people died of lung injuries caused by a steriliser sold by Reckitt which was put inside humidifiers; a £300 million charge has been taken in relation to the tragic episode.

While South Korea, Russia and Brazil are challenged markets, Reckitt is internationally diversified, seeing strength in India, China and Turkey for instance, and Shares is sticking with our positive stance – see Plays, 17 Mar 2016. Reckitt’s health, hygiene and home portfolio is spearheaded by enviable ‘Powerbrands’ including Nurofen, Strepsils, Gaviscon, Durex, Scholl, Cillit Bang and Air Wick, which confer pricing power and underpin Reckitt’s dependable cash flows and reliably progressive dividend.

Pricing power

Pricing power is a sign of a great business, though as the ‘Marmitegate’ spat between Unilever (ULVR) and Tesco (TSCO) showed, hiking prices isn’t easy in the current retail environment. Sterling’s slump is driving up the costs of imports to Britain at a time when consumer goods firms face fierce competition from retailers’ own-brand products and weaker emerging markets. Nevertheless, we’re in agreement with the generally bullish consensus on Reckitt.

Liberum Capital maintained its ‘buy’ and £84 price target following the Q3 update and even upgraded its 2016 earnings per share estimate given a tailwind from sterling weakness and support from share buy-backs. Transforming into a global powerhouse in consumer health, Liberum argues relentless innovator Reckitt has scope to double turnover in ten years as it benefits from strong secular growth trends coupled with M&A. For 2016, the broker forecasts pre-tax profit of £2.731 billion (2015: £2.341 billion) for earnings of 295.1p, rising to £3.128 billion and 344.4p respectively in 2017. The shareholder reward is forecast to rise from 139p to 149.8p this year ahead of a 174.8p payout next. (JC)

A pullback from July highs to £72.63 presents a buying opportunity at Reckitt, a global consumer health colossus with brand strength and pricing power, though some may still find the rating overly rich.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.