Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

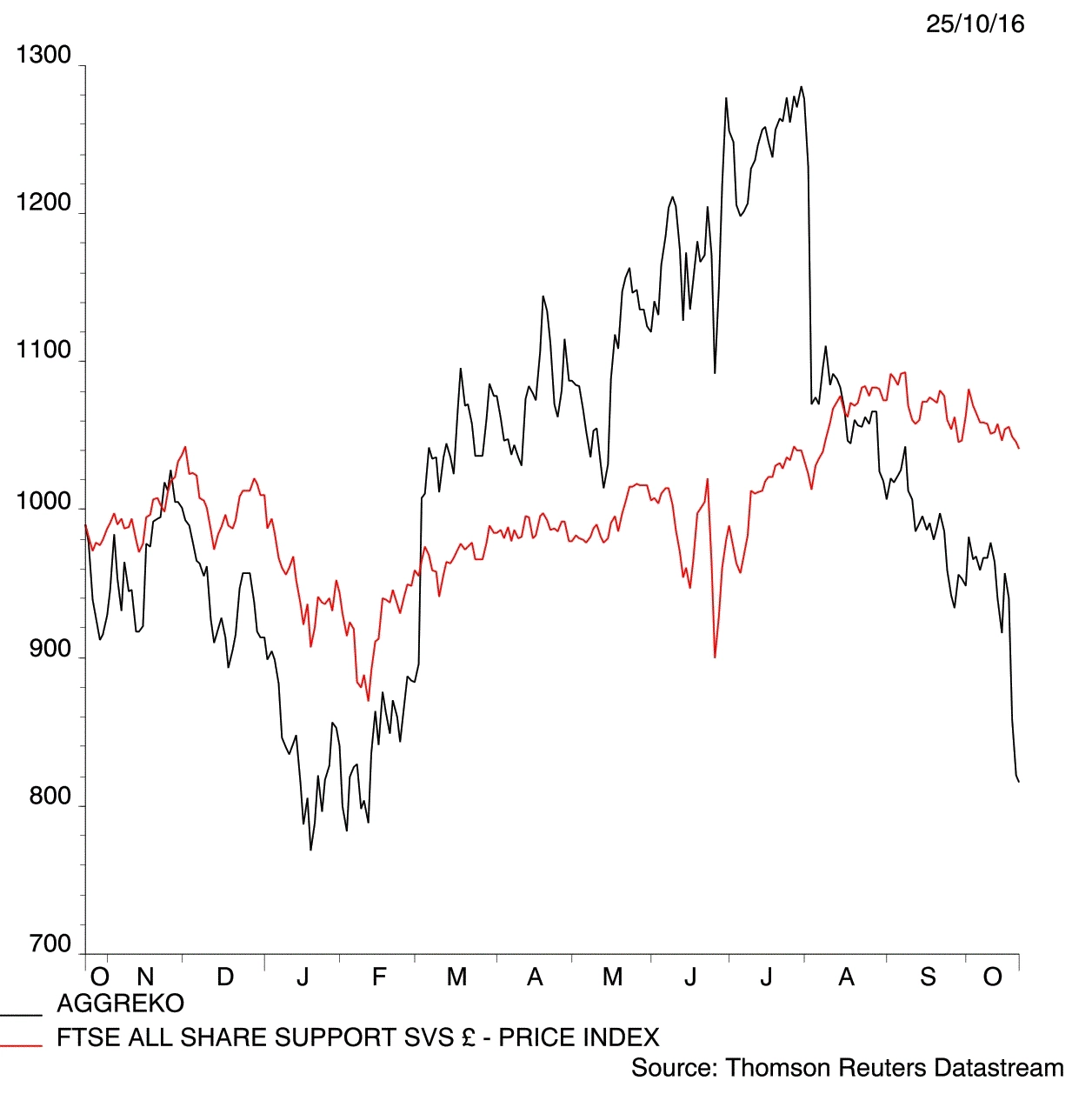

magazineAggreko hit by Panmure ‘sell’ note

Mobile power generation provider Aggreko (AGK) slumps 15% as Panmure Gordon analyst Michael Donnelly slaps a ‘sell’ rating on the stock. We think the outlook is more positive for a stock which is one of our top picks for 2016.

Donnelly, who flagged concerns about Utilitywise (UTW:AIM) and Capita (CPI) ahead of similar sell-offs, says low growth, struggling end markets and poor cash conversion are Aggreko’s key problems.

Aggreko is now in its fourth year of ‘effectively zero growth’ writes Donnelly. Revenue growth is important, according to Donnelly’s analysis, if management is to achieve a return on capital target of 20%.

End markets are also struggling, Donnelly adds, flagging 40% of profit earned in North America, Latin America and Africa as potentially at risk from lower renewable energy prices and competition.

Finally, Donnelly says the stock is ‘very expensive’ on a calendar year 2017 free cash flow yield of 5.3% and a dividend yield of 2.9%.

Arguing a more bullish case in August, Aggreko chief executive Chris Weston said Aggreko’s fleet on hire in Utilities, its largest and most profitable division, is expected to head towards 85% of capacity later this year. That would be the highest since 2012 and lead to material year-over-year gains in revenue and margins moving into 2017.

Donnelly’s earnings per share estimate in 2016 is 65p, rising to 74p the year after. Shares in Aggreko trade at 816p.

If this is the bearish case on Aggreko investors should actually be fairly encouraged.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.