Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow fund managers apply a fuel injection

Investment trusts have a trick up their sleeve in their effort to enhance shareholder returns. ‘Gearing’ involves a fund manager using debt to invest in more companies or other assets and boost the value of a portfolio. It creates a bigger pool from which to earn dividends and/or generate capital gains.

The term ‘gearing’ often appears on financial literature, but is seldom understood by investors. We now explain how it works, what it means for your wallet and reveal some investment trusts using this as a tool to turbo charge returns.

This is how gearing works

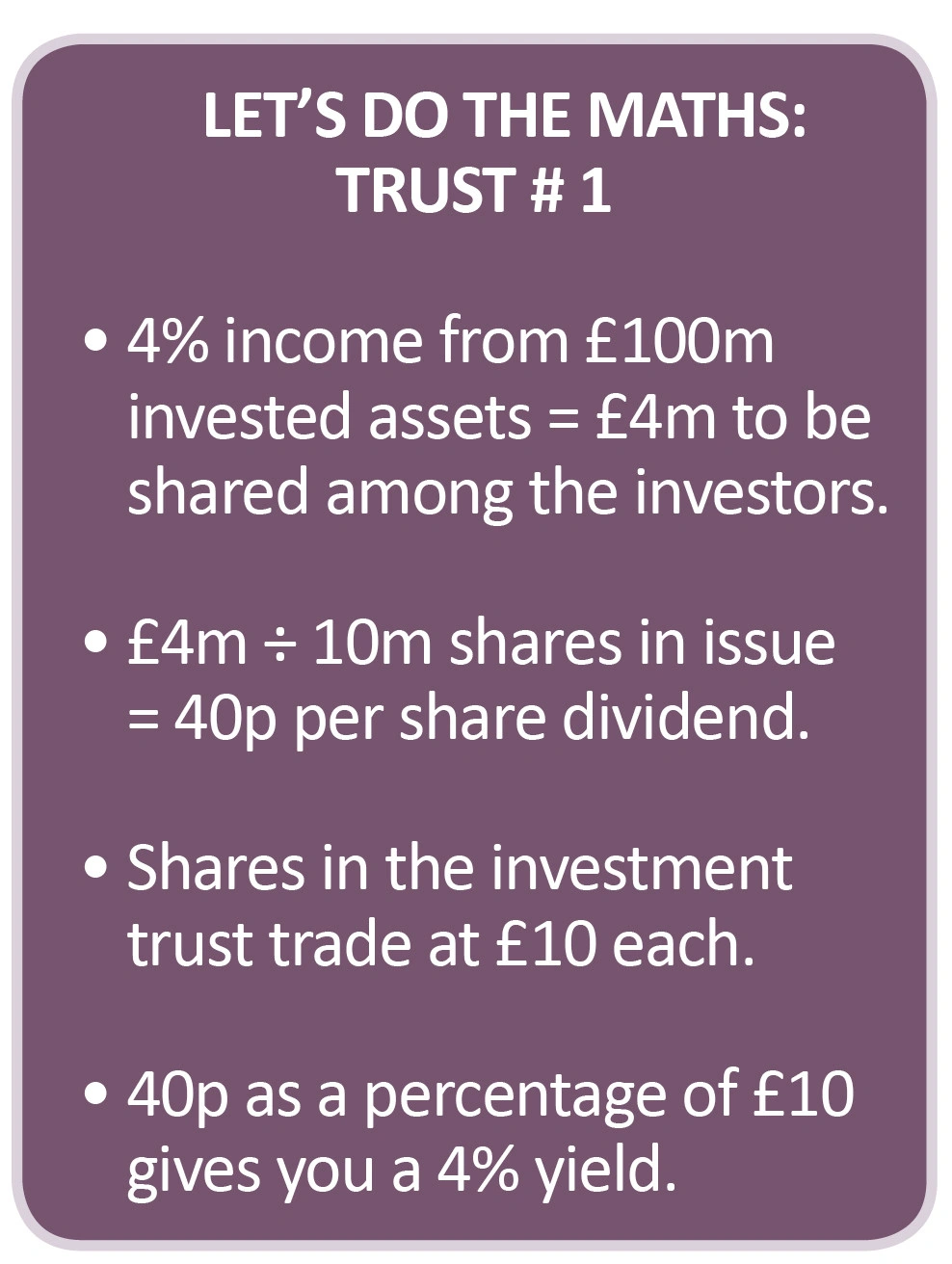

We have created two hypothetical investment trusts as a way of illustrating the concept of gearing.

Trust #1 has £100m invested in a range of different companies and 10m shares in issue. The underlying holdings in the portfolio pay dividends to the trust which it then distributes to shareholders.

Let’s say the investment trust earns 4% annual income from its underlying holdings. It passes all of that money to shareholders.

Trust #2 also has £100m invested in a portfolio of companies. It decides to borrow money equivalent to 15% of its portfolio to have an extra £15m to invest in more companies. That is what’s referred to as gearing.

The investment portfolio now totals £115m.

Does gearing push up the share price?

You mustn’t presume the share price will be inflated by 15% to reflect the extra cash suddenly in the trust’s account. The net asset value is still £100m. The share price tends to be influenced by net asset value.

Net asset value, or NAV, is assets minus liabilities. In this case it would be £115m investment assets minus £15m debt liabilities = £100m.

The only scenario where the cash injection might influence the price is if market sentiment is negative towards stocks and investment trusts with debt, so a discount might be applied.

The same applies if sentiment is positive and so investors put a higher price on the trust because they think it is going to make higher returns.

For purposes of our illustration, we assume no change to the share price. The dividend calculation will be based on the invested assets, which in this case is £115m.

We will assume the portfolio of companies generates the same 4% annual income for the investment trust and that there are 10m shares in issue.

You can see how the use of gearing has enhanced the dividend yield on the second investment trust.

This is a simple explanation of gearing. The calculations do not factor in any cash held in reserve to help smooth dividend payments in more difficult market conditions. Neither do the calculations include fund management charges.

Buy more stuff

Gearing is a useful tool for the fund manager as it means they don’t always have to sell holdings when they find something else in which they’d like to make an investment.

The fund manager needs to be confident they can earn a better return on the additional investments than the cost of borrowing the money.

There are different methods by which a fund manager can gear up a portfolio including bank debt, loan stock, debentures, foreign currency loans or preference shares.

Gearing can enhance portfolio returns yet it can also magnify losses in negative market conditions.

(Click on table to enlarge)

They can't go crazy

Investment trusts normally follow a pre-defined gearing strategy which is published on their website or in financial reports. For example, the board might say the fund manager is allowed to use up to 10% gearing. The fund manager needs to keep within the range agreed by the board of directors.

Temple Bar Investment Trust (TMPL) says it can go as high as 50% with its gearing but adds that a more normal range is 0% to 30%.

Blue Planet Investment Trust (BLP) can go to 75% gearing but is presently at just under half this level at 33.4%. There are plenty of investment trusts which choose to have no gearing at all. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.