Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine‘Electric cars are good for GKN’

Automotive engineer GKN (GKN) needs to shout louder about its opportunity in electric-powered vehicles, according to Panmure Gordon analyst Sanjay Jha.

GKN, which is set to deliver a third quarter trading update on 25 October, held a dinner with analysts in September to talk about its Driveline division.

‘Last night, I witnessed the first signs of excitement from the company on electrification of cars even though most of the energy was coming from Michigan-based senior vice president Dr Ray Kuczera,’ wrote Jha.

‘If GKN was a US company it would have finished the analyst presentation with a table-thumping slogan. Instead it ended with “electrification is good for GKN”.’

GKN’s Driveline business has a ‘great opportunity’, Jha says, because new entrants into the electric vehicles market are more likely to outsource production than existing manufacturers. Smaller and more complex than standard vehicles, e-vehicle drivelines also deliver higher than average margins.

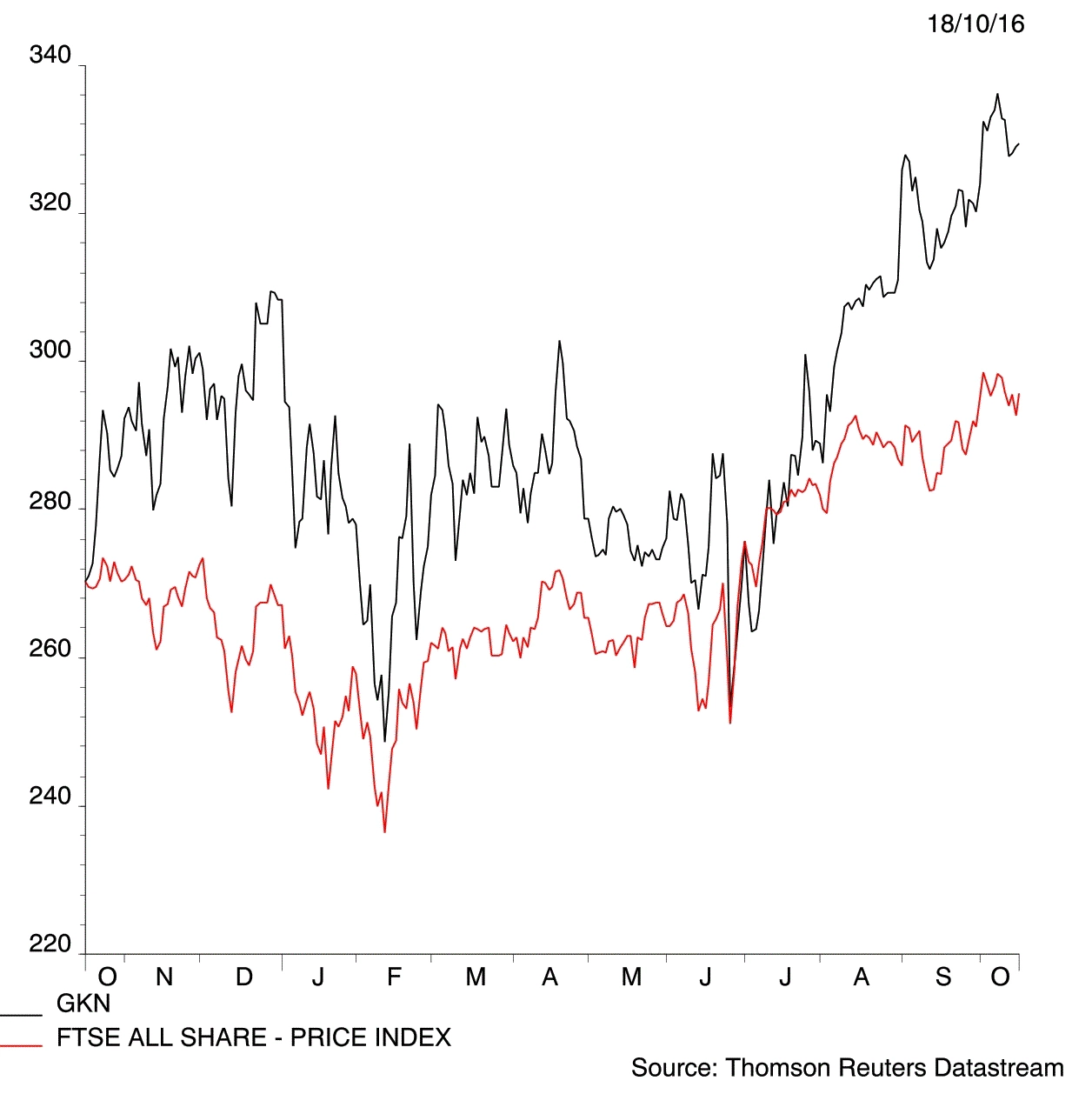

Opportunities in GKN’s Driveline unit are offset by the group’s £2.1bn pension deficit, which is a key risk for investors. Jha estimates sales in 2016 will come in at around £9bn, pre-tax profit at £683m and earnings per share at 29.4p. GKN’s shares trade at 329p. (WC)

Even with a large pension deficit this looks like a good business.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.