Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine5 stocks Buffett would buy now

Investors aiming for big returns on the stock market can learn a lot from the Berkshire Hathaway (BRKA:NYSE) business model built by legendary investor Warren Buffett.

We’ve spotted several companies on the UK market that meet the criteria he desires in an investment. Read on and you’ll discover the names he would theoretically want to buy.

WHO IS BERKSHIRE HATHAWAY?

Berkshire Hathaway is an American conglomerate business run by Buffett. In 2014 and 2015, Berkshire earned about as much from its wholly-owned utilities businesses as it did from its stock market investments.

Looking at Berkshire Hathaway’s performance is an education in how to pick stocks as well as how to build a solid, well-diversified portfolio.

Berkshire Hathaway’s four main divisions are focused on insurance, utilities, manufacturing and services and financial products.

Importantly, Buffett argues ‘there are important and enduring economic advantages’ to owning all of these four very different divisions within one business.

WHAT DOES THIS MEAN?

Partly, it means drivers of profitability across these four divisions are very different.

If Berkshire suffers large insurance losses in one year, it is possible one of its other divisions will deliver stronger performance to offset them.

‘If the insurance industry should experience a $250bn loss from some mega-catastrophe – a loss of about triple anything it has ever experienced – Berkshire as a whole would likely record a significant profit for the year because of its many streams of earnings,’ wrote Buffett in a 2015 shareholder letter.

When economies go through a soft patch and general business activity is slow, insurance and utilities companies are capable of delivering solid profits when other sectors struggle.

Stronger periods of economic growth should see Berkshire’s manufacturing and services and financial products businesses register more impressive performance while Utilities and Insurance plod along.

'Some of our picks look expensive on current forecasts. Longer term they have low risk growth drives. This means they may still be incredibly cheap'

APPLY BUFFETT’S GENIUS TO YOUR PORTFOLIO

There are several companies on the UK market that meet the criteria Buffett desires in an investment.

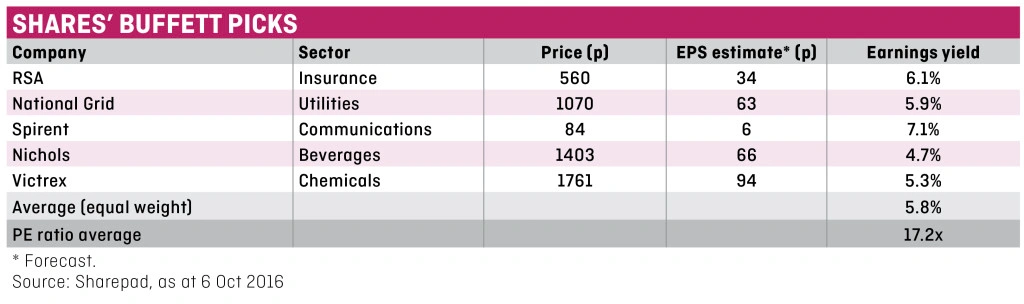

We’ve selected five stocks from this list that fit into Berkshire’s three main investment categories: insurance, utilities and manufacturing and services.

Our key pick in insurance is RSA (RSA), a good quality general insurer in the midst of a turnaround which could deliver substantial shareholder value.

In utilities, options are limited in the UK: we’ve singled out National Grid (NG.). As well as defensive qualities, National Grid has a few investment catalysts on the horizon in the near-term.

Manufacturing and services is the area where Buffett’s policy of buying wonderful businesses at reasonable prices is most apparent.

(Click on table to enlarge)

Our top picks in this section are Spirent (SPT), soft drinks brand owner Nichols (NICL:AIM) and speciality chemicals outfit Victrex (VCT).

Trading at an average price-to-earnings (PE) ratio of 17.2 these stocks are expensive based on this year’s earnings forecasts. Longer term, all have relatively low risk growth drivers, in our view. This means they may still be incredibly cheap.

Why Buffett likes

INSURANCE

Insurance has been the engine of growth at Berkshire Hathaway ever since Buffett bought a quirky business called National Indemnity in 1967 for $8.6m.

Headed by maverick businessman Jack Ringwalt it insured circus performers and lion tamers, among others. Today, under the Berkshire umbrella, it is the largest property-casualty insurer in the world.

Property-casualty insurance is a key part of Berkshire’s business though it is important to note Buffett is not as keen on life insurance companies, which are very different businesses.

So why does Buffett like insurance? Two attractions of the property-casualty insurance industry are the ‘free money’ it generates, known as insurance float, and an unusual earnings profile which may add diversification to an equity portfolio.

We’ve chosen RSA as our preferred UK-listed non-life insurance stock as management initiatives have helped the business return to what are now sustainable profits, in our view.

‘FREE MONEY’

Insurance companies, like Berkshire’s National Indemnity, generate free money.

Payments from customers to insurance companies for products like home or auto insurance are paid up-front. Claims, however, only have to be paid out in the future.

In the interval between when a customer pays an insurance premium and when they make a claim, insurance companies have access to capital at zero cost.

Float builds up as an insurance company writes more premiums: Berkshire’s float, thanks in part to National Indemnity’s growth, now totals around $90bn.

As long as Berkshire writes a similar amount of insurance each year, it is able to hold on to and invest what is essentially its customers’ cash in assets for itself.

Berkshire’s equity and bond portfolios are mainly funded by this unusual and highly valuable source of capital.

On top of investment returns earned from investing insurance float, the industry tries to make money from underwriting, though this is not always the case.

Underwriting profit is earned when an insurer’s premium income from customers exceeds the amount it pays out in claims and other operating costs, like staff salaries and administration.

DIVERSIFICATION BENEFIT

Property-casualty insurance companies’ earnings should not be affected too much by the general economy, so neither should their share prices.

Insurance is a not just a necessity but also a legal requirement in many cases and while customers may shop around more in hard times, auto and home insurance in particular enjoy fairly stable demand.

Provided insurance companies attract good quality customers, price their policies correctly and invest insurance float conservatively they should make money in most economic environments.

Diversification benefits provided by insurance companies may reduce risk in a portfolio and could be one reason why Buffett likes the insurance industry.

RSA (RSA) 562p

Market cap: £5.7bn

Progress on a management turnaround plan at RSA and the potential for further profit improvements are two reasons for investors to check out the pet cover-to-commercial insurance writer.

A third quarter trading update scheduled for 3 November could prove to be a further catalyst at RSA if improvements outlined in the first half of the year continue to be delivered.

Run by former Royal Bank of Scotland (RBS) chief executive Stephen Hester, the insurer is selling underperforming assets and trying to improve a key measure of profitability, RSA’s combined ratio.

An insurer’s combined ratio shows how much money it is making from ordinary insurance policies, before including returns on investment activities.

RSA’s combined ratio declined from 96.4% to 94.1% in the first half of 2016. A number below 100% shows the business is making a profit from insurance underwriting.

Investment returns, another key source of earnings for insurers, were also better than expected because lower interest rates increased the value of its bonds. Investment grade bonds represent more than 80% of RSA’s £14.5bn portfolio.

Consensus analyst estimates are for earnings per share of 33.5p in 2016 and 42.2p in 2017.

Why Buffett likes

UTILITIES

Earnings from Berkshire Hathaway’s wholly-owned utilities businesses contributed almost a third of its profit in 2015.

Railroad Burlington Northern Sante Fe, purchased by Berkshire in November 2009, is by far the largest of its utility assets, followed by energy utilities in North America and the UK.

REGULATED MONOPOLIES

Railroads must be maintained at great expense to keep freight moving around the US while ongoing investment in energy infrastructure is vital to keep businesses and households supplied with reliable power.

‘We relish making such investments as long as they promise reasonable returns – and, on that front, we put a large amount of trust in future regulation,’ wrote Buffett in Berkshire’s 2015 shareholder letter.

‘Our confidence is justified both by our past experience and the knowledge that society will forever need huge investments in both transportation and energy.’

'Society will forever need huge investments in both transportation and energy'

BOND-LIKE CASH FLOWS

Utilities are regulated by governments to ensure they do not seek to exploit monopolies of supply at the expense of other businesses and households.

Regulated profitability removes, justifiably, some of the upside for investors in monopolies.

Downside risk to profitability at utilities is also typically low, however, meaning cash flows are very stable over time.

Utilities as a result have a performance profile similar to bonds and their profitability is usually not affected too much by economic cycles.

National Grid (NG.) £10.69

Market cap: £40.3bn

Power transmission network National Grid offers a good, defensive portfolio diversifier for investors pursuing more eye-catching gains elsewhere – a strategy Buffett uses at Berkshire Hathaway.

An all-weather business that should deliver even in tough economic conditions, National Grid also has a couple of near-term investment catalysts.

First, it is selling a stake in its gas distribution network which analysts estimate is worth £12bn in total. This could lead to a special dividend of around 40p a share sometime in 2017.

Second, National Grid has North American assets which contribute around 30% of operating profit. Management has struggled to make the most of this business and there could be upside to earnings per share if profitability improves over the period to 2020, as expected.

Risks include lower future dividend cover as the gas distribution stake sale will reduce earnings. Consensus earnings per share forecasts for the year to 31 March 2017 are 63p and 64p in 2017. Forecast dividends at 44p imply a yield of 4.1%.

Investors preferring more diversified exposure to utilities could consider iShares Global Infrastructure ETF (INFR) which is full of utilities including National Grid. Half the fund is allocated to US utilities and infrastructure assets.

How does Buffett

PICK STOCKS?

Berkshire Hathaway’s manufacturing and services division and stock market portfolio are the area where chairman Warren Buffett is best known for working his magic.

Defensive qualities provided by Berkshire’s large investments in the utilities and insurance sectors mean Buffett can afford to be more adventurous in other areas.

Buffett’s policy of buying high quality businesses at reasonable prices – both on the stock market and from private owners – is one of the main reasons Berkshire’s long-term returns exceed the S&P 500 index by 10% per year since 1965.

It makes sense investors seeking better-than-average returns to look for better-than-average businesses like those Berkshire owns outside its insurance and utilities units.

Reasonable profit margins, low debt and high and sustainable returns on equity are key features.

We now explain what Buffett means when he talks about investing in ‘wonderful businesses at reasonable prices’.

WHAT IS A WONDERFUL BUSINESS?

Berkshire Hathaway’s manufacturing and service business unit includes a number of companies which Buffett has bought outright from private owners or, occasionally, from the stock market. Key attributes include:

1. REASONABLE MARGINS

Operating profit margins are a measure of the percentage profit a company earns per dollar of revenue.

High profit margins are often a sign of better quality businesses.

Berkshire Hathaway’s manufacturing and services division boasts reasonable though not stand-out margins, at around 7%.

All three of our UK stock picks deliver operating margins above this level.

2. SENSIBLE BALANCE SHEET

Berkshire Hathaway as a whole and its manufacturing and services business division as a group carry no significant levels of net debt.

Businesses listed on the stock market usually carry some debt because it can increase shareholder returns.

Debt is not usually a problem provided the amount relative to equity and to earnings is reasonable. In this case, we’ve opted for three stocks which all had more cash than debt on their balance sheets at their last year-end.

3. SUSTAINABLE RETURNS ON EQUITY

Businesses which can deliver high returns on equity (RoE), measured as profit divided by the difference between assets and liabilities (book value), are usually considered high quality.

Berkshire Hathaway’s manufacturing and services division delivered a pre-tax RoE of 12.5% in 2015.

It is impressive given Berkshire’s businesses employ very little debt or other forms of leverage, which tend to magnify return on equity.

Trailing 12 month returns on equity among our stocks picks are around 3.6% at Spirent, which we expect to improve significantly; 35% at Nichols; and 23% at Victrex.

Buffett’s preference for companies with strong brands and pricing power are also features of his investing approach. To a large extent these features are captured within the aforementioned key financial ratios, in our view. (WC)

Stocks that tick the right boxes

for BUFFETT

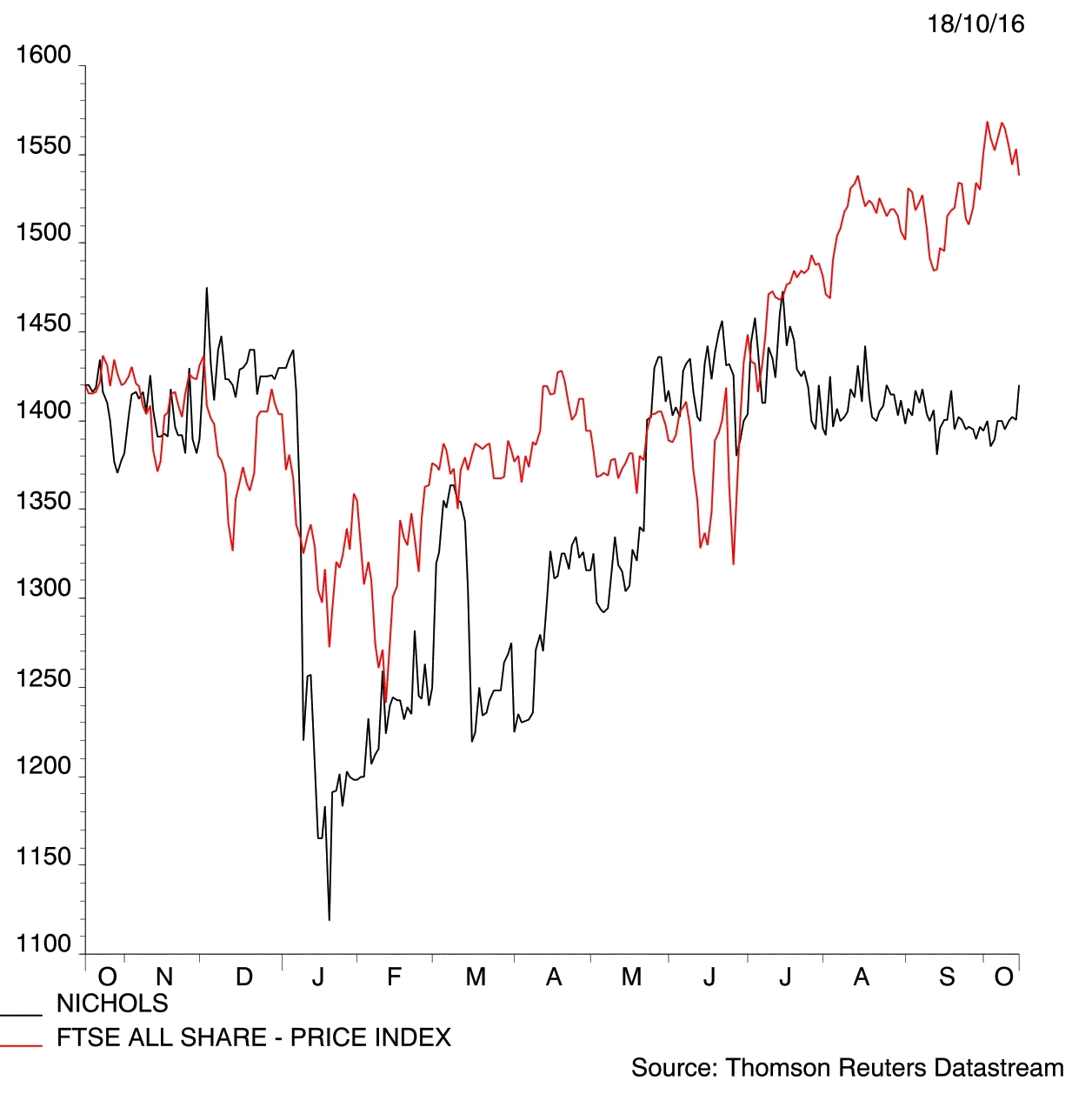

Nichols (NICL:AIM) £14.03

Market cap: £518m

A range of highly profitable niche soft drink brands which

sell all over the world and a rock solid balance sheet give Nichols its star quality.

Key brands Vimto, Levi Roots, Sunkist and Panda are consumer favourites in some key geographies.

While Nichols competes against some formidable rivals in the beverages market its smaller scale has some advantages.

Acquisitions of up-and-coming brands can enhance Nichols’ profitability significantly but would not move the dial at multi-billion dollar companies like Coca-Cola (KO.:NYSE).

Recent deals include the purchase of premium juices outfit Feel Good and iced drinks specialist the Noisy Drinks Co. Both boosted earnings in the half year to 30 June 2016. Even after the deals, Nichols recorded balance sheet cash of £33m.

Risks include a tough UK soft drinks market, a proposed UK sugar tax and competition from larger rivals. (JC)

Victrex (VCT) £17.61

Market cap: £1.5bn

Manufacturer of polyether ether ketone (PEEK) products, Victrex is a Berkshire Hathaway-quality business as measured by its high profit margin and return on equity, coupled with a conservative balance sheet and good market position.

Invented by ICI in 1978, PEEK is a plastic used in aerospace, automotive and electronics markets because of its light weight, durability and strength. Victrex was created as the business to exploit the new technology.

From £17m of sales in 1993, Victrex delivered revenue of £263.5m in 2015 with operating margins of 40% and return on equity at 23%.

Analysts at Liberum say Victrex is selling into an addressable market with future potential demand at seven times today’s capacity. Risks include competition from larger rival Solvay (SOLB:EBR). (WC)

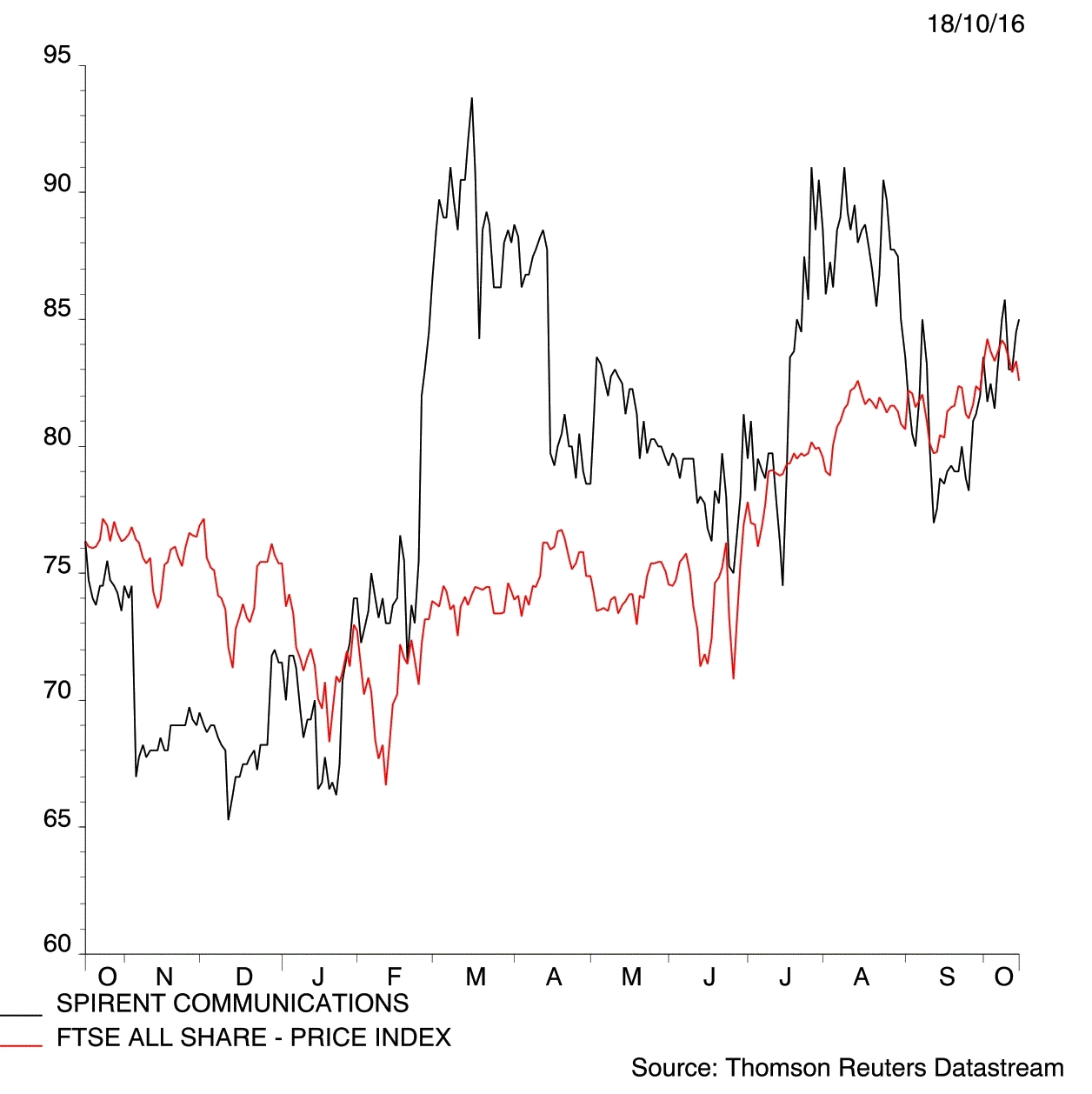

Spirent Communications (SPT) 84p

Market cap: £512m

A global supplier of testing and performance measurement equipment to the telecoms industry, Spirent’s aim is to deliver around 50% of its forecast $540m (£443 million) sales from recurring sources, as opposed to one-off contract revenues, by the end of 2018.

Spirent’s peak operating margin in 2011 was close to 25% providing a glimpse of what could be possible as a corporate turnaround gathers pace. Analysts currently forecast margins of 11.4% in 2018.

On a 2017 price-to-earnings (PE) multiple of 11.8, Spirent trades at a large discount to historic PEs in the low 20s. Firmer evidence of improving profits could bring the double-whammy of a re-rating on top of earnings curve benefits. (SFr)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.