Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe scramble For dividends in Asia is just getting started

In the West the grasp for yield has become a protracted theme for investors. Income hungry, they have been forced to search in non-traditional income-yielding asset classes as bond yields continue their fall amid the flow of central bank money from across the globe.

The UK government now rewards you a mere 0.6% a year if you lend to them for 10 years. In Germany you’ll need to pay the government to take your money. As the risk-reward dynamic has become skewed, income-yielding equities have never been more en-vogue.

Looking East

Investors have tended to focus chiefly on income yielding equities originating in western markets; places where they believe companies are transparent, democratic, well governed, and focused on the value they provide shareholders.

But high quality companies can be found elsewhere around the globe. According to Henderson’s dividend index monitor – a study tracking the progress of the top 1,200 companies by market capitalisation in growing their dividends – over a trillion dollars of dividends were paid out in 2015.

While it is true that North American, European and UK companies made up around $750bn of this figure, companies from Asia Pacific and Japan dolled-out a handsome $162bn.

It marks a shift: Asian companies have been, for some time, changing their approach to shareholders, driven top-down by governments wishing to improve capital distribution, increase efficiency and attract a larger stable of global investors.

Korea, for example, is levying penalties on companies who hoard too much cash on their balance sheets; the emphasis of reform in China’s state-owned enterprises (SOE) has been to refocus management towards shareholder returns.

Japan – Asia’s champion and the second largest equity market in the world – echoes the shift. In the summer of 2013 Japan Exchange Group and Nikkei Inc. developed the JPX-Nikkei 400. The index frees itself from the traditions of weighting by market capitalisation (market value of a company) to include measures such as the company’s profitability or corporate governance structures.

The aim is to improve capital distribution to drive efficiency and attract a larger stable of global investors, marking a permanent structural shift towards Asia’s own ‘dividend culture’.

High yield for a reason

Due to the perceived risks, yields in Asia have traditionally been much higher than that of the West. This has changed in recent years as yields have fallen. So what does this signify?

In the past, heavyweight Asian investors such as large pension funds and sovereign wealth funds have tended to allocate their cash towards fixed income assets and property. This made sense. With yields significantly higher than Western markets, exposure to the additional capital risk in equities would have been nonsensical.

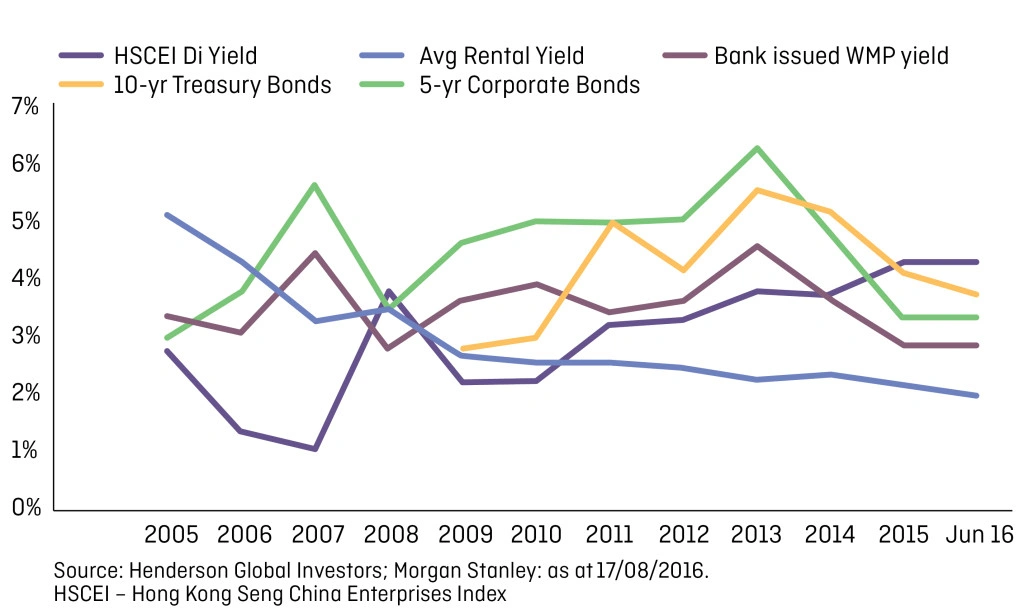

Recent evidence points to a shifting landscape in this regard. Look at data from China, the region’s stalwart economy, and you’ll see yields have been steadily dropping across a number of income asset classes: government bonds, corporate bonds, property, and even wealth management products.

The latter offer fixed-term pay-outs based on underlying assets and have been hugely popular among retail investors.

Some of the non-bank wealth management products offered fairly high (and unsustainable) yields in the past due to the spurious assets underpinning them, and are now facing a government clampdown.

Similar products sponsored by banks are deemed safer, but yields have contracted to below 4%. That is also lower than the yield of the main H-Shares equity market in Hong Kong (HSCEI) and a growing number of shares listed in Shanghai and Shenzhen, China, a far less compelling proposition than 12 months ago.

Overall, the effect has been to squeeze all of the traditional avenues for income, making equity yields – rising on account of the improving corporate attitudes towards shareholders and increasing pay-out ratios (the percentage of net income paid out as dividends) – an increasingly attractive income proposition on a risk / reward basis. The picture is reflected across most Asian markets.

How are investors reacting?

Institutional investors, cognizant of the eroding value in traditional income asset classes, have been changing their allocations towards equities for the first time in history.

In Taiwan the risk-based capital requirements for insurers and pension funds have been raised, which could attract between $25bn and $35bn towards equities over the next five years.

Singapore’s sovereign wealth fund, GIC, is in talks to buy 7% of Vietcombank in Vietnam. In India, the biggest retirement manager has recently been permitted to invest 5% to 15% of new assets in equities, where before they had not been allowed.

The tendency has been for dividend paying stocks with low betas – those of lower volatility when compared with the wider market. A market capitalisation weighted index of 44 Asian stocks with dividends above 3% and betas of between 0.8 - 1.0 (less than one implies lower volatility than the market; more than one implies greater) has been climbing, especially since the Bank of Japan introduced negative interest rates.

A wholesale change?

Thus far, the steps towards Asian equity income have only been tentative. In Thailand 17% of the top pension funds have assets in stocks, compared with 61% in Hong Kong, according to the Organisation for Economic Cooperation and Development (OECD).

It is the demand potential from retail investors that could be game-changing. As a percentage of Gross Domestic Product (GDP), China has a savings rate of 49% versus a world aggregate of 24%, a US rate of 18%, and 12% in the UK, according to the World Bank.

With China’s GDP at around $11trn, the savings portion is eye-watering. And with savers receiving the same lacklustre yields as institutional investors even a small allocation switch has the potential to move significant sums of cash into the equity markets. It paints a picture of potentially rampant domestic Asian equity demand.

In our portfolios the strategy has been to provide a blend of income yielding equities with lower yielding equities with the potential for dividend growth. We believe this mix – with improving corporate governance and attitudes towards shareholder value and dividend pay-outs – provides our investors the opportunity to diversify their income stream, particularly for those invested in UK markets where the majority of dividends are paid by only a handful of companies (in the UK the top 10 companies in the FTSE 100 pay 57% of the entire market’s dividends). The change afoot in Asian markets is only just getting started.

Before investing in an investment trust referred to in this article, you should satisfy yourself as to its suitability and the risks involved, you may wish to consult a financial adviser.

The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Nothing in this article is intended to or should be construed as advice. This article is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment.

Issued in the UK by Henderson Investment Funds Limited (reg. no. 2678531), incorporated and registered in England and Wales with registered office at 201 Bishopsgate, London EC2M 3AE, is authorised and regulated by the Financial Conduct Authority to provide investment products and services.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.