Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

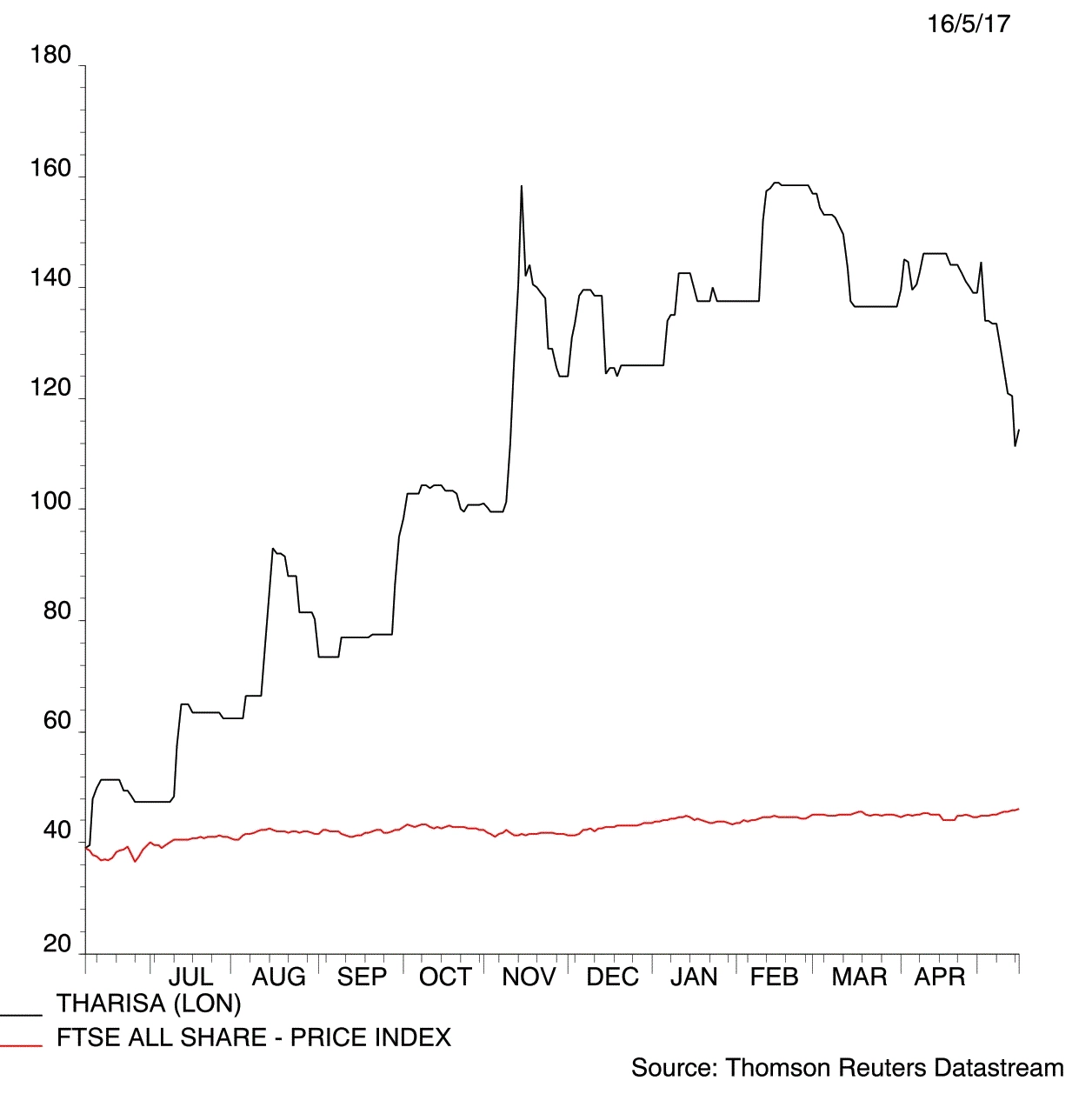

magazineGreat Ideas update: Tharisa

Tharisa (THS) 103.75p

Gain to date: 33.9%

Previous Shares view: Buy at 77.5p, 29 September 2016

Better-than-expected platinum group metals (PGMs) production has helped to lift shares in miner Tharisa (THS). The stock is now up 33.9% since we said to buy a fortnight ago.

Tharisa extracts PGMs and chrome from its mine in South Africa and sells them to China. A bullish trading update on 10 October says PGM recovery rates from its mine were higher than targeted and tons milled reached a record high. It also states that metallurgical grade chrome prices have risen by 50% in the third quarter of 2016.

These factors bode well for Tharisa’s upcoming full year results which will be published on 29 November 2016. The company has also confirmed to Shares that it intends to recommend a maiden dividend at these results.

Dividends could become a key part of the investment case in the future. Tharisa has a low cost mine with the potential to generate significant amount of cash.

Stockbroker Peel Hunt implies that its 120p price target may prove too conservative. (DC)

Keep buying the shares despite the strong run that’s already taken place. Tharisa is really cheap on a mere 4.6 times 2017 forecast earnings

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.