Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“Lower loan impairments as the pandemic’s impact starts to ease, prudent lending policies and a new online portal all mean that specialist finance provider S&U is making the most of an upturn in demand for both cars and property refurbishments in the UK,” says AJ Bell investment director, Russ Mould.

“Profits are up, the dividend is growing again after last year’s setback and the increase in receivables shows that the FTSE Small Cap company is already laying foundations for future growth.

“As a result the shares are already trading within touching distance of their all-time high but on a forward price/earnings multiple of 15 with a twice-covered dividend yield of around 3.5% the stock may yet appeal to investors who seek capital appreciation or income alike.

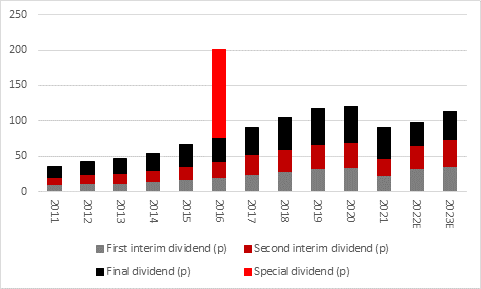

“S&U traditionally pays two interim dividends a year, one in November and one in March, followed by a final payment in July. Chairman of the board, Anthony Coombs, has declared a first interim distribution of 33p a share, compared to 22p a year ago. That looks to firmly underpin analysts’ consensus forecasts for a total dividend of 98p a share for the year to January 2022, compared to 90p a year ago, and even hints that estimate is a little conservative.

Source: Company accounts, Marketscreener, consensus analysts' forecasts. Financial year to January.

“That is still below the pre-pandemic peak of 120p a share but new loan advances in excess of £115 million, compared to just £60.6 million in the first half of the last fiscal year, shows that S&U is already generating fresh momentum in its two niches.

“Through its Advantage Finance arm, the Solihull-headquartered firm provides non-prime loans for cars, while the fledgling Aspen Bridging operation offers property loans for individuals and commercial borrowers, who wish to purchase or refurbish an asset.

“Some investors may share the big banks’ reticence to get involved, if they have concerns over the UK economy and its car and property markets in particular. Loan-loss provisions did rise at S&U last year as the pandemic hit and a downturn in the UK economy and any associated jump in unemployment could jeopardise customers’ ability to repay their loans.

“However, S&U does manage risk in a disciplined manner, as you would expect of a company that dates back to 1938 and can point to three generations of management by the founding family, which still has a major shareholding.

“Moreover, both of those markets are currently showing signs of a strong recovery after 2020’s woes. The market for nearly-new used cars is booming, amid a shortage of new vehicles, and Aspen, while only approving a small percentage of applications, is building a strong loan book and future pipeline.

“Even as group-wide payments collections rose sharply, total receivables across both arms of the company rose 9% year-on-year to £306 million, a new high for the firm.

Source: Company accounts, Marketscreener, consensus analysts' forecasts. Financial year to January.

“Pre-tax profit is already rebounding quickly and strong end demand, coupled with skilled underwriting, could lead to further increases and in turn fund both further investment in the business and dividends. In addition, the company has the ability to borrow up to £180 million from its own lenders and with just £115 million of those facilities already deployed, S&U has a further £65 million available for growth.

Source: Company accounts, Marketscreener, consensus analysts' forecasts. Financial year to January.

“S&U’s first-half pre-tax profit of £19.9 million exceeds the sum earned across the whole of the last financial year (£18.1 million) and again suggests that analysts’ forecasts for 2022 and 2023 are potentially conservative – meaning that the shares may be cheaper than they look, on an earnings basis, assuming that the wheels do not fall off the UK economy in the meantime. Consensus estimates are currently looking for pre-tax profit of £28 million for the year to January 2022 and £33.3 million for 2023.”

These articles are for information purposes only and are not a personal recommendation or advice.

Related content

- Wed, 24/04/2024 - 10:37

- Thu, 18/04/2024 - 12:13

- Thu, 11/04/2024 - 15:01

- Wed, 03/04/2024 - 10:06

- Tue, 26/03/2024 - 16:05