Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“An increase in the dividend, a decrease in debt and no change to profits expectations for the year would read well at most firms, especially in the current environment and particularly at Imperial Brands, after its torrid run of profit earnings disappointment, dividend cuts and management changes,” says AJ Bell Investment Director, Russ Mould.

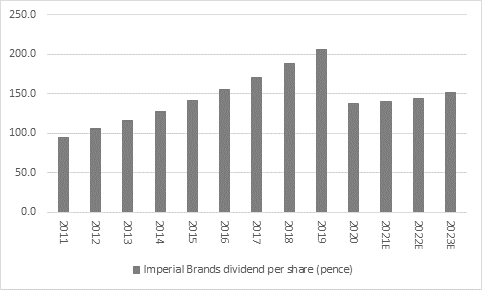

“The 1% increase in the interim dividend to 42.12p a share might not sound much but it helps to underpin consensus analysts’ forecasts of an 8.6% dividend yield from Imperial Brands’ stock this year, the third-highest figure in the FTSE 100.

Source: Company accounts

“Investors will be breathing more easily after the increases in revenues, operating profit and earnings per share in the first half. Comments from CEO Stefan Bomhard about stabilising market share in tobacco in key markets, lower losses from Next Generation Products thanks to more controlled investment and firm pricing will also offer encouragement.

“A 5.3% average price increase probably exemplifies the one single reason that investors hold tobacco stocks – pricing power. Pricing power underpins margins which underpins cash flow which underpins dividends and after last year’s dramatic cut, analysts are pencilling in small but steady increments in the shareholder distribution once more.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

“However, cash flow was not as strong as last year, thanks to a reversal of last year’s cash inflow from distribution business Logista. Other challenges also lie ahead, including the impact of tax increases in Australia on 1 September 2020, the ongoing loss of duty-free business at airports and the absence of certain covid-19 related benefits last year.

| £ million | 2016 | 2017 | 2018 | 2019 | 2020 | H1 2021 |

|---|---|---|---|---|---|---|

| Operating profit | 2,229 | 2,278 | 2,407 | 2,197 | 2,731 | 3,592 |

| Depreciation & amortisation | 1,244 | 1,364 | 1,266 | 1,316 | 910 | 1,637 |

| Net working capital | 138 | 67 | (11) | 50 | 1,042 | 372 |

| Capital expenditure | (217) | (235) | (327) | (409) | (302) | (1,331) |

| Operating Cash Flow | 3,394 | 3,474 | 3,335 | 3,154 | 4,381 | (91) |

| Tax | (401) | (570) | (407) | (522) | (568) | (431) |

| Interest | (540) | (537) | (491) | (473) | (420) | (255) |

| Pension contribution | (111) | (157) | (60) | (72) | (88) | (73) |

| Leases paid | 0 | 0 | 0 | 0 | (72) | (38) |

| Free Cash Flow | 2,342 | 2,210 | 2,377 | 2,087 | 3,233 | (210) |

| Dividend | 1,386 | 1,528 | 1,676 | 1,844 | 1,753 | 906 |

| Free Cash Flow Cover | 1.69 x | 1.45 x | 1.42 x | 1.13 x | 1.84 x | (0.23 x) |

Source: Company accounts

“Shareholders will also be watching the progress of the proposed Tobacco Tax Equity Act in America, The Democratic Party’s latest initiative, which would raise federal levies on tobacco products, comes after suggestions that President Biden’s party will also look at legislation designed to lower the nicotine content in cigarettes, in addition to re-examining a possible ban on menthol-flavoured products.

“Yet long-term shareholders in Imperial Brands (and British American Tobacco for that matter) will know that bills to raise tax on tobacco are launched just about every year in America - and they generally falter. The Democratic Party itself seems divided on the issue and Republicans support looks unlikely. Even if the Republicans do help, the implementation of any law may be years away. In addition, history suggests that the big tobacco firms are quite capable of raising prices to offset any tax hit that comes their way, an impression only reinforced by these first-half results from Imperial Brands.

“These risks remain real, nonetheless – but that is why the shares trade on a forward price earnings ratio of less than ten and offer a yield of 8.6%. Investors are paying low multiples and demanding a lofty yield to compensate themselves for the potential dangers involved, so the valuation goes at least some way to pricing in the numerous challenges which the tobacco industry still faces.

| Dividend yield (%) 2021E | Dividend cover (x) 2021E | Pay-out ratio (%) 2021E | |

|---|---|---|---|

| Rio Tinto | 9.0% | 1.30 x | 77% |

| Evraz | 8.8% | 1.44 x | 69% |

| Imperial Brands | 8.6% | 1.29 x | 77% |

| M & G | 7.7% | 1.15 x | 87% |

| British American Tobacco | 7.7% | 1.58 x | 63% |

| Persimmon | 7.5% | 1.02 x | 98% |

| Polymetal | 7.2% | 1.53 x | 65% |

| BHP Group | 7.2% | 1.21 x | 82% |

| Admiral Group | 6.7% | 1.02 x | 99% |

| Phoenix Group | 6.5% | 0.54 x | 185% |

Source: Marketscreener, consensus analysts’ forecasts, Refinitiv data

“Investors who run rigorous environmental, social and governance (ESG) screens before they select a share will not even consider tobacco stocks for portfolio inclusion and long-term worries over the trend in cigarette volumes in the face of regulatory pushback could undeniably limit the potential for capital appreciation from shares in tobacco firms.

“But income-seekers may yet get their dividends and that might help to put some sort of floor under the shares, which are holding firm this year at least in the face of the proposed US law-making activity, covid-19 and continued pressure from both the tax and medical authorities.”

These articles are for information purposes only and are not a personal recommendation or advice.

Related content

- Wed, 24/04/2024 - 10:37

- Thu, 18/04/2024 - 12:13

- Thu, 11/04/2024 - 15:01

- Wed, 03/04/2024 - 10:06

- Tue, 26/03/2024 - 16:05